ING Viewpoint August 2020

Tanate Phutrakul, CFO of ING Group

"Central bank digital currency (CBDC) is a challenging concept and it is still early days. A lot of choices regarding its goals, design, and implementation still need to be made. We see opportunities for CBDC, but also a number of inherent challenges.

CBDC is not simply about finding an optimal technical solution for digital payments. Rather, It is a fundamental reconsideration of the roles of money, central banks, and the financial sector. Because the payment infrastructure is the backbone of the economy and the financial system, any changes should be considered carefully. At ING we stand ready to engage in a constructive dialogue with our key stakeholders on this important topic."

Tanate Phutrakul, CFO of ING Group

Introduction

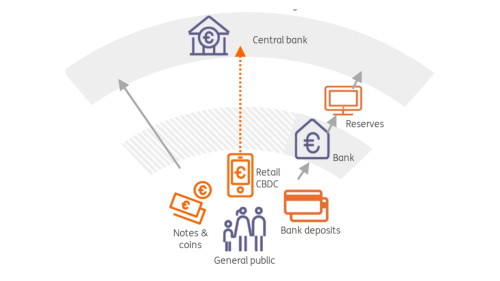

Today, citizens can hold money basically in two forms: in the form of physical cash, issued by central banks, or in the form of deposits with banks. Over the past decades the use of bank deposits has outgrown physical cash - the latter constitutes less than 10% of money in circulation in the eurozone. Bank deposits serve as a vital source of funding for the other major financial-economic function of banks: extending credit to businesses, households and the public sector.

In the digital age, CBDC can be considered a “third way” between physical cash and digital bank money. CBDC would allow citizens to retain access to central bank issued money (like physical cash), but in a digital form (like bank deposits; see figure below). A retail CBDC would thus secure a strong public sector presence in the digital money landscape. A retail CBDC may compete with (or even replace) bank deposits, which may reduce and destabilise the deposit funding available to banks. This would in turn affect their ability to lend.

CBDC is part of a broader spectrum of possible digital currencies. Bitcoin is the best known one. Various “ stablecoin ” initiatives seek to benefit from decentralised bookkeeping and other innovations but bring challenges, being privately issued and requiring some value stabilisation mechanism. The arrival of such initiatives, alongside other jurisdictions exploring CBDC, means that the EU is wise to consider innovative options to increase the international relevance of the euro, maintain monetary sovereignty and safeguard the financial system. A euro CBDC might be a way forward.

This viewpoint discusses the main opportunities and challenges of CBDC. The potential impact of CBDC is substantial, ranging from changing payment infrastructures to availability and pricing of loans and the composition of Europe’s digital finance markets.

With this viewpoint, ING aims to contribute to the reflections on CBDC in Europe.

Different forms of money: cash, bank deposits and CBDC

Retail CBDC would introduce a new digital way for the public to hold money, bypassing banks. This is illustrated by the shaded area, indicating a potential servicing role for banks (similar to cash distribution via ATMs), but no balance sheet commitment ("disintermediation"). See our Research publication "Will central banks go digital?" for more background information.

Ongoing initiatives

A global central bank working group (including ECB and Sweden’s Riksbank ) is exploring potential CBDC use cases.

The People’s Bank of China is piloting a Yuan retail CBDC.

The Banque de France’s focus until now has been on wholesale CBDC.

The Bundesbank is taking a cautious approach.

De Nederlandsche Bank published an exploratory paper on retail CBDC in an EU context.

CBDC can create opportunities...

It is important to distinguish retail from wholesale CBDC. The latter is restricted to financial institutions, and its main aim is to increase efficiency of wholesale payments. This viewpoint focuses on retail CBDC. An often-asked question is "but what problem does it solve?". Here are some potential answers:

Declining use of physical cash: CBDC could provide an alternative digital means for the public to retain access to central bank issued money in the digital age, without the central bank having to build the IT infrastructure to host millions of account holders. We believe there is limited economic justification for this argument, particularly where commercial bank deposits are safeguarded by insurance schemes. Yet for some, this is not about economic rationale but rather about the principle that citizens can access central bank money without going through intermediaries.

Safeguarding monetary sovereignty: the prospect of successful privately issued currencies stablecoins ” such as Facebook’s Libra) as well as public sector digital currency initiatives elsewhere in the world have raised a variety of concerns. These include fair competition, platform dependence, security, financial stability, monetary policy transmission and the use of digital currency as a geostrategic tool. European authorities may therefore prefer to stay in control.

Technological innovation: creating a new payments infrastructure from scratch may produce efficiency gains and make it easier to incorporate new features such as programmable money and smart contracts. At the same time, many innovative features can also be (and are already being) incorporated into existing payment infrastructures as well.

Financial inclusion: similar to a bank account, CBDC will require a digital device and (digital) identity verification. Yet it might contribute to bringing digital payments to the underbanked in some countries.

New tools for central banks: CBDC could make it easier to fine-tune monetary policy by applying different rates for different holders of CBDC ( e.g., consumers and businesses).

... but also poses challenges that need to be addressed

As an active contributor to innovation in the payment area, ING welcomes new possibilities unlocked by technology. Yet CBDC would change the foundations of our current monetary and payment infrastructure, so policymakers should carefully consider its key political and economic implications.

Financial stability: retail CBDC would provide the public with an alternative to bank deposits. This would force a reconsideration of banks’ role in society. The availability of CBDC could facilitate bank runs, but also structurally deprive banks of an important source of funding and therefore reduce their ability to provide credit. Retail deposits are a more stable source of funding than short-term loans from capital markets, which is why deposits become an even more important source for bank credit during crises.

Regardless of whether commercial bank disintermediation as a result of CBDC is good or bad, it entails systemic financial stability risks. Central banks are aware of this but proposed solutions may fall short. For example, imposing limits upon individuals’ CBDC holdings might invite political pressure in times of crisis. Alternatively, central banks may commit to funding banks indefinitely. This may be an undesirable blurring of public and private sector roles.Monetary stability should also be considered. Widespread availability and accessibility of CBDC could exacerbate international capital flight to safe haven CBDC during crises. This is problematic for the safe haven jurisdictions involved, as it could exacerbate overvaluation of their currency. For crisis-hit emerging markets, it could intensify currency collapse, with all social consequences attached to it.

Competition and supervision: depending on the setup chosen, a CBDC might create direct competition between central banks and private parties. Central banks might also embark on activities they normally supervise themselves. Neither situation is desirable, and care should be taken to avoid them.

We believe that a better approach would be to take the public-private partnership in physical cash as a blueprint, with distinct roles and tasks for either part, e.g. in the areas of AML, duty of care, and (cyber)risk management.

In addition, where CBDC is distributed by both (commercial) banks and non-bank service providers, it is important that the same set of rules applies to both.

Conclusion

We welcome explorations into CBDC. At the same time, retail CBDC in particular is a potentially very disruptive innovation, demanding careful consideration on a technical, social, and political level.

Key issues to be addressed include financial stability, supervisory responsibilities, the division of labour between the public and private sectors, and the terms of competition among private CBDC service providers.

As an innovative institution, we welcome the opportunity to engage constructively

with policymakers and the central bank community on the opportunities as well as challenges of this emerging technology.