State aid for ING: the facts and figures

During the credit crisis ING, like other banks, received aid from the government. Here’s a round-up of all the facts and figures.

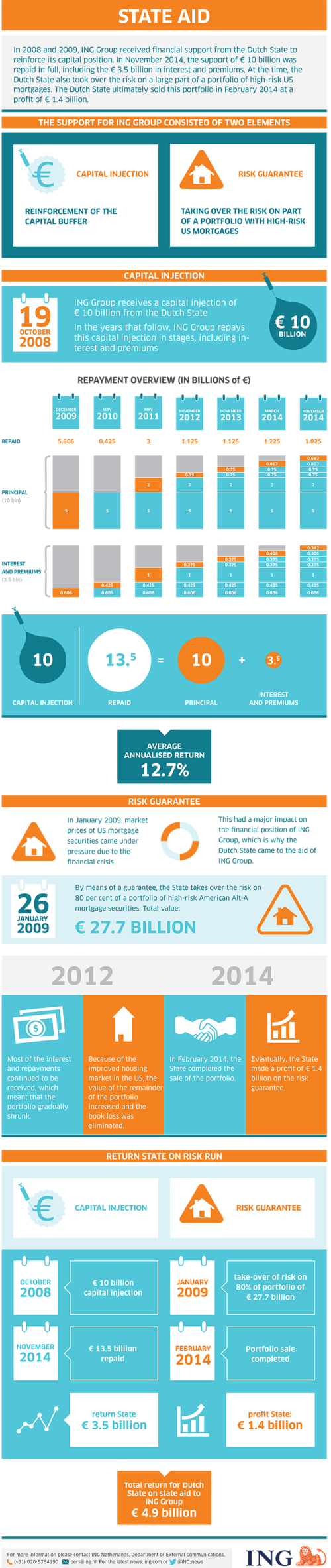

In October 2008 and January 2009 ING received support from the government. The aid to the banks has consequences for Dutch taxpayers, but the support given to ING also yields revenue for the State. We regularly get questions about this. So here is a rundown on all the facts and figures about the ING state aid.

October 2008: capital injection

Amidst the unrest that ensued after the collapse of the US merchant bank Lehman Brothers in September 2008, the perception arose around the world that banks needed more buffer capital. That’s why the Dutch government decided on 9 October 2008 to make € 20 billion available in order to help fundamentally healthy financial institutions strengthen their capital.

On 19 October 2008 ING Group became the first to make use of this support in the form of a capital injection of € 10 billion. As part of the deal ING agreed to pay a premium of up to 50% upon the repayment of this loan. ING is only required to pay interest on the aid if dividend is paid out to ordinary shareholders. In this case, ING will pay at least 8.5% interest.

January 2009: Back-up Facility for Alt-A mortgage portfolio

On 26 January 2009 ING Group and the Ministry of Finance announced that the Dutch State would take over the risk on 80% of a large package of so-called US Alt-A mortgage bonds.

In 2012 the value of the Alt-A portfolio crept steadily higher thanks to a slightly more favourable economic tide in the US. The ‘break-even price’ fell, which made these bonds easier to sell. The Dutch State can benefit from a good return; since December 2012 the Dutch State is in a position to sell the Alt-A portfolio in the market at a handsome profit.

ING announced on 6 February 2014 that, together with the Dutch State, it had completed the unwinding of the Illiquid Assets Back-Up Facility (IABF), which was announced in November 2013. The Dutch State has sold the remaining USD 11.5 billion of securities in the portfolio through three auctions for an average price of 77,3%. The proceeds were used to pay off the remaining loans from ING. Together with the settlement of fees, the unwinding resulted in a cash profit for the Dutch State of EUR 1.4 billion.

Restructuring: a key condition for state aid

To obtain approval from the European Commission for state aid during a financial crisis, enterprises are usually required to draw up a restructuring plan, which must also ensure that the state aid does not give them an unfair competitive advantage.

ING, too, must demonstrate that it can continue operating in the future without government subsidies and that the State receives sufficient compensation for its support. These requirements have had far-reaching consequences for ING. Among other things, ING was compelled to drastically reduce its activities and separate its banking and insurance operations. A large part of this process has already been completed.

Capital injection payments and repayments

ING began repaying the Dutch State in December 2009 and completed its final payment in November 2014. All payments were approved by the Nederlandsche Bank (DNB), the Dutch central bank. The total amount repaid to the Dutch State on the core Tier 1 securities was EUR 13.5 billion, including EUR 10 billion in principal and EUR 3.5 billion in interest and premiums, giving the State an annualised return of 12.7%.

ING’s payments to the Dutch State were as follows:

- On 12 May 2009, ING paid an initial interest coupon of EUR 425 million.

- In December 2009, ING repurchased the first half of the core Tier 1 securities of EUR 5 billion plus a total premium of EUR 606 million.

- On 13 May 2011, ING exercised its option for early repurchase of EUR 2 billion. The total payment in May 2011 amounted to EUR 3 billion and included a 50% repurchase premium.

- On 19 November 2012, ING announced that, together with the Dutch State, it reached an agreement with the European Commission on significant amendments to the 2009 Restructuring Plan. As part of the agreement, ING filed a schedule for repayment to the Dutch State of the remaining EUR 3 billion in core Tier 1 securities plus a 50% premium, in four equal tranches in the next three years.

- The actual payments were:

- A first tranche of EUR 1.125 billion was paid on 26 November 2012;

- A second tranche of EUR 1.125 billion was paid on 6 November 2013;

- A third tranche of EUR 1.225 billion was paid on 31 March 2014;

- The final tranche of EUR 1.025 billion was paid on 7 November 2014, half a year ahead of the repayment schedule as agreed with the European Commission in 2012. This final payment was also approved by the European Central Bank.

Where is the money coming from?

The money for the payments to the State broadly comes from three sources: the shareholders, the operating profit and the proceeds from the sale of business assets. In 2009 shareholders put € 7.5 billion into ING via a rights issue. The majority of this amount was used to repay the State.

In the past years ING also made a profit. This was used for the further reinforcement of the capital, but also partly to repay the state aid. Since 2008 the shareholders have not received a share in the profits in the form of a dividend. In addition, ING has sold some of its business assets. This yielded a profit in certain cases, which also enabled ING to strengthen its capital and repay the State.

More information about Transactions with the Dutch State.

The State aid background in one infographic