ING Viewpoint July 2019

Ralph Hamers, CEO ING Group

“Digitalisation is blurring the boundaries between sectors and within financial services.

Longstanding well-defined banking functions such as payments, saving and borrowing are being unbundled and combined in new ways. New market entrants, fintechs, play a crucial role in building a more innovative financial sector.

At the same time, established banks look beyond traditional practices and launch their own fintech challengers. The benefit is better, more personalised financial services against lower costs.

The innovation that underpins these market developments also fosters financial inclusion, enabling financial institutions to support market segments that have historically been difficult to access.

To fully reap the benefits of innovation, consistent and proportionate application of regulatory and supervisory requirements is needed.”

Ralph Hamers, CEO ING Group

Both businesses and policymakers are adjusting to new digital realities that affect financial services at a fundamental level. We see the EU’s main role as creating a stable and appropriate regulatory environment that allows innovation to thrive regardless of where it takes place. To that end, the framework for digital financial services needs to be updated through:

- Addressing supervisory fragmentation at the EU level to support Europe’s fintech ecosystem and to tackle financial stability and integrity challenges arising from unbundling of banking services. Supervision at EU level is needed.

- Facilitating innovation by established institutions through a tailored supervisory regime for internal innovation projects that pose no financial risks for the parent bank.

Addressing supervisory fragmentation to support Europe’s fintech ecosystem

New market entrants have transformed banking. Traditional bank services are being unbundled and the payments and finance business optimised to deliver targeted, highly-specialised financial services in a more customer-friendly and cost-efficient way. By focusing only on small pieces of the financial services value chain and outsourcing the rest, fintechs often do not fall under the same supervisory requirements as traditional banking.

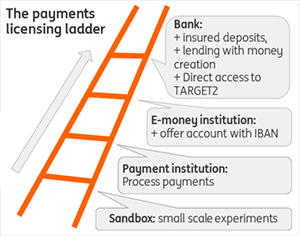

Taking the payments sector as an example, a payments start-up is usually launched under a regulatory sandbox regime that is operated by a national supervisor and then scaled up via various licencing regimes in accordance with the EU regulatory framework.

A “licensing ladder” which starts with a payment services provider evolving into an e-money institution, then to a partially licensed bank (e.g. including deposit-taking but excluding lending) and finally to a fully licensed bank accommodates innovation while maintaining financial stability and integrity.

We believe that such a proportionate, activity-based licensing framework that gradually increases regulatory requirements as a firm’s services expand, creates both a conducive enabling environment for new market entrants and a level playing field for established banks.

The supervision of banking, payments and e-money institutions and the way licenses are granted, however, differ across Europe. The banking regime resides at EU level with the European Central Bank (ECB) as single supervisor, while payments and e-money institutions are nationally licensed and supervised. Such nationally licensed and supervised institutions can offer their services in other Member States by using the EU’s passporting system. This creates a risk of supervisory fragmentation or even supervisory competition, which increases as fintechs concentrating on specific services outsource non-core parts of their business to third parties (including banks). This growing trend has led to the emergence of a complex network of interconnected financial institutions offering services across Europe, while supervision is fragmented along national borders.

This supervisory fragmentation may, as fintechs and bigtechs gain importance, impact Europe-wide systemic financial stability, regulatory compliance and consumer protection. Efforts should be made to harmonise not only the regulatory framework, but also the supervision of payments and e-money institutions at EU level to ensure that responsibility is borne by the right actors in the value chain, and that any systemic and non-financial risks are identified and addressed accordingly.

How to stimulate innovation within banks

Incumbent banks innovate at least as much as new market entrants. Many of the world’s leading banks have launched their own internal innovation labs to test and develop emerging technologies. As part of the banking group, however, these innovation projects are subject to the full supervisory regime, including:

- All prudential and conduct rules stemming from the banking license. The deposit-taking role of banks justifies stringent regulatory requirements to ensure financial stability;

- Internal controls and risk policies, validated by supervisors. The extent to which internal policies apply is predominantly determined by banks themselves. In applying these policies, banks tend to err on the side of caution to avoid inadvertently breaking any law.

Whilst banks’ innovation projects can be included in regulatory sandbox regimes, they remain subject to more direct supervisory oversight and stringent regulatory requirements than those of their non-bank competitors, who are licensed and subsequently supervised based only on their activity.

Banks’ internal innovation projects could be supported if they could take a step down the “licensing ladder” discussed earlier, and be subject to a supervisory regime that is more akin to the framework applied to their non-bank competitors. Such an approach would honour the principle of “same services, same risks, same rules”. It would be a proportionate, activity-based element embedded in the banking supervisory regime. Of course, “stepping down the licensing ladder” should only be allowed if the innovation project poses no prudential risks to the parent bank, subject to the supervisor’s assessment and approval.

This supervisory discretion could apply across the different stages of innovation. For instance, when banks launch their innovation projects under a regulatory sandbox, supervisors could make use of their discretionary powers to further reduce the supervisory burden. Such a regime would enhance the sandbox that is already available in many jurisdictions and make it more useful for incumbent banks. To avoid fragmentation along national borders, an augmented sandbox framework would work best if it were standardised across the EU.

As internal projects scale up, they leave the sandbox. For projects that are dependent on or tightly integrated into the bank’s operations, notably in terms of critical infrastructure, brand or distribution channels, it is clear that the full banking license and internal policies need to apply.

However, for projects that do not pose risks to the stability of the bank, a lighter regime one step down the “licensing ladder” would be more appropriate and should be possible. Such a regime would facilitate the scaling up of banks’ internal fintech activities. The current regulatory framework does not offer banks and supervisors an option to apply a comparable supervisory regime to innovation projects by moving them down the “licensing ladder”.

The only option banks currently have to reduce the supervisory burden on their fintech activities, is to put them at arm’s length, not only financially, but also in governance terms. Only then can a project, under certain conditions, be exempted from the parent banking license and apply for its own license. This, however, does not allow the parent bank to maintain control over its fintech activities. Control is important for innovation to contribute to the bank’s digital strategy and business priorities.

Supervisors’ caution in reducing the regulatory requirements on banks is understandable: they serve crucial functions in society and should, in all circumstances, be safe. Yet at the same time, creating room for innovation both outside and inside banks, is necessary for the European economy to prosper. We appreciate this is a very complex issue. We advocate a review of the governance framework to enable a tailored supervisory regime for banks’ innovation projects, conditional on them being sufficiently remote from the parent bank in prudential terms. Such a regime would enable banks to integrate innovation into their own business model, invest more in innovative scale-ups for the benefit of consumers and compete with fintechs and bigtechs on equal terms.

Conclusion

EU policymakers should consider making targeted changes to the regulatory and supervisory framework for financial services that will help attain the broader objective of stimulating innovation while ensuring consumer protection and financial stability. Addressing the risks that arise from the unbundling of financial services and facilitating innovation by both fintechs and established banks will ensure a level playing field to the benefit of consumers and strengthen the EU’s fintech ecosystem. Furthermore, creating regulatory room for banks to move their innovation projects a step down the “licensing ladder” will greatly stimulate innovation.