ING Viewpoint

Ralph Hamers

CEO and Chairman,

ING Group

“The Banking Union is a significant step forward tackling systemic risk in the Euro-area. However, there is room to move to more coordination on macro-prudential policy.

Micro-prudential supervision and bank resolution are now firmly established in the hands of Banking Union institutions. A Single Resolution Fund was set up and negotiations are ongoing to establish a Eurozone wide Deposit Insurance Scheme. To complete the Banking Union, criteria for macro-prudential policy need to be harmonised and overseen by the Eurozone’s bank supervisor, the ECB. This ensures risks being addressed at an appropriate and consistent level and banks competing on a level playing field.”

Ralph Hamers

CEO and Chairman, ING Group

Executive Summary

The Banking Union project, and other sweeping regulatory changes after the financial crisis, have made the Eurozone’s banking sector more resilient. However, the Banking Union framework provides only a limited framework to address macro-prudential risk in a coordinated and harmonised manner.

The ECB, as the Eurozone’s banking supervisor, should be given the mandate to play a stronger coordinating role to harmonise criteria for macro-prudential policy. While we recognise that macro-prudential policy addressing idiosyncratic risks should be executed at the national level, we are of the view that the ECB should be able to set a common methodology for national authorities to use these tools.

This will allow the Banking Union to further improve resilience of the Eurozone by consistently addressing macro-prudential risk; and guard the level playing field between competing banks in the Banking Union. This should be addressed as part of the EU’s macro-prudential framework review.

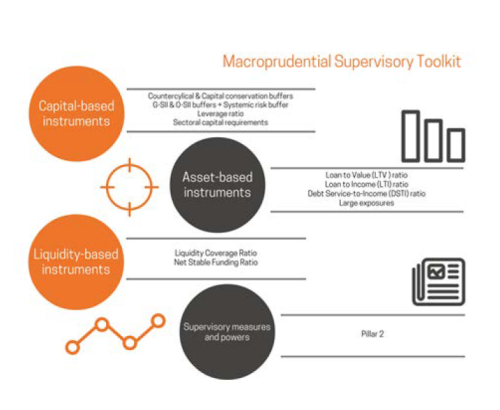

Macro-prudential policy: what it is, what it does and who decides

The establishment of the Banking Union introduced a new era in bank supervision where genuine considerations for financial stability are meant to go beyond the national context and powers of national authorities have become more harmonised across the Euro area. The post-crisis framework has rightfully established a wider set of macro-prudential tools to address financial stability risks alongside micro-prudential supervision built around risk-based capital requirements.

Macro-prudential policy aims to address system-wide risks stemming from diverse sources such as the financial cycle, the interconnectedness of the bank system or the stability of the financial system as a whole. There are two main types of macro-prudential tools: macro-prudential capital buffers, allowing for increases in overall capital requirements, and portfolio-specific instruments, notably to tackle the build-up of cyclical risk in the real-estate sector.

In the Banking Union both national supervisors and the European Central Bank (ECB), coordinating with the EU-wide Systemic Risk Board (ESRB), are responsible for setting macro-prudential policies. Domestic authorities are responsible for setting and implementing macro-prudential measures in their markets while the ECB has an oversight role and can increase these requirements if there are risks to the financial stability. However, whilst the ECB has gained strong powers over microprudential supervision, it does not have an overall mandate to coordinate and harmonise methodologies guiding macro-prudential policy in the Banking Union and its Member States.

Banking Union calls for strong coordination of macro-prudential tools in the Eurozone …

The Banking Union was created to break the bank-sovereign risk nexus in the Euro area with the objective to sever the dangerous link between the health of the sovereign and its banking system. Entrusting supervision and resolution to the Single Supervisory System (SSM) vested in the ECB and the Single Resolution Board (SRB) respectively has put the Eurozone on the right path.

Since there can be circumstances warranting country-specific actions, national authorities should remain primarily in charge of executing such policies.

Nonetheless a deeper harmonisation of how macro-prudential policy is set is justified at Eurozone level. The ECB setting out consistent methodologies, supplemented with the local knowledge of national supervisors about emerging risks, would institutionalise a common rationale for applying macro-prudential policy consistently in the Banking Union.

More broadly, the Banking Union would benefit from more clarity, predictability and transparency regarding crucial banking regulation. Harmonised methods that make macro-prudential policy more predictable can facilitate adequate pricing of risks by bank investors and avoid unwarranted uncertainty in financial markets.

This will in turn strengthen the credibility of Europe’s bank resolution regime and the credibility of the system’s resilience as a whole.

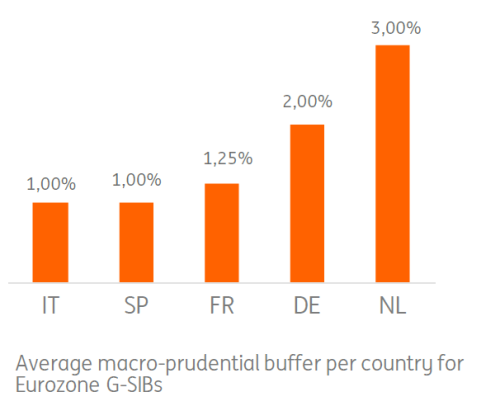

... harmonising the methodology is paramount to maintain a level playing field between banks

Non-harmonised macro-prudential rules, be it on setting the buffers or the portfolio specific instruments, can lead to banks with similar risk profiles experiencing significantly different regulatory requirements in the markets in which they operate.

Increasing capital requirements are not neutral in terms of funding costs. Banks would need to compensate by re-pricing their products, notably by increasing loan margins or lowering interest rates on deposits. Therefore, if macro-prudential policies are not applied consistently, it is possible that banks with identical risk profiles face significantly different product pricing conditions, thereby creating an undue distortion of the level playing field.

Establishing a level playing field is at the heart of the Banking Union project: within Banking Union similar banks in risk and profile should face the same regulatory treatment.

This will allow strong banks to compete across the Eurozone, and can mitigate the sovereign-bank feedback loop which had been so harmful during the high of the Eurozone crisis.

Non-harmonised macro-prudential rules, be it on setting the buffers or the portfolio specific instruments, can lead to banks with similar risk profiles experiencing significantly different regulatory requirements in the markets in which they operate.

Increasing capital requirements are not neutral in terms of funding costs. Banks would need to compensate by re-pricing their products, notably by increasing loan margins or lowering interest rates on deposits. Therefore, if macro-prudential policies are not applied consistently, it is possible that banks with identical risk profiles face significantly different product pricing conditions, thereby creating an undue distortion of the level playing field.

Establishing a level playing field is at the heart of the Banking Union project: within Banking Union similar banks in risk and profile should face the same regulatory treatment.

This will allow strong banks to compete across the Eurozone, and can mitigate the sovereign-bank feedback loop which had been so harmful during the high of the Eurozone crisis.

Macro-prudential buffers should not be set in a vacuum …

The currently ongoing work on risk reduction measures should be evaluated alongside macro-prudential buffers, as it addresses overlapping risks. For example, a macro-prudential buffer based on a bank-size to GDP ratio will be less relevant as the Eurozone’s bank resolution regime and its funding will definitively no longer be national in nature.

The Eurozone’s banking system has doubled capital requirements, addressed liquidity outflow risks and established a resolution system designed to prevent public bail-outs. Loss absorbency requirements have been introduced and eff-orts are underway to address residual ‘too-big-to-fail’ risk in the financial system as well as proposed constraints to the use of internal models and the introduction of capital floors.

We expect this to result in significant increases in both the risk weighting of assets and overall capital requirements.

... and needs to reviewed on a continuing basis under criteria developed by the ECB

The ECB has a central role to play in coordination with national authorities to review how macro-prudential policy plays a role vis-à-vis other supervisory measures. Such an exercise will need robust substantiation and needs to be established under criteria set by the ECB and will require an ongoing assessment.

A stronger ECB role over macro-prudential policy can create synergies with micro-prudential supervision to better counter the emergence of financial vulnerabilities.

It will also help to spot any duplicative or unintended interaction between the application of different micro and macro-prudential tools.

Conclusions

- Macro-prudential policy today would benefit from greater harmonisation to ensure consistent application in a Banking Union context. The ECB as the Eurozone’s banking supervisor is best placed to ensure a strong coordination over how macro-prudential tools are set and applied.

- Centralised harmonisation of macro-prudential measures is necessary to avoid an unlevel playing field between Eurozone banks and set more clarity and predictability on how they are implemented through a revision of the current macroprudential framework.

- The framework and the role of different regulators, will need to be based on robust criteria set centrally by the ECB. It will need to spot any undue interaction between different tools and take account of the risk reduction.