ING Viewpoint November 2016

Koos Timmermans

Vice-Chairman

Management Board Banking

“Europe is making good progress implementing the Banking Union. But the past years have taught us that banks cannot and should not serve the financial needs of the economy all by themselves. That is why Europe needs a Capital Markets Union alongside the Banking Union. A revised framework for the securitisation market is an essential part of the Capital Markets Union. A well-functioning market will unlock additional sources of financing for Europe's enterprises and private individuals and will stimulate economic growth. For investors and savers, it could enhance returns.”

Koos Timmermans,

Vice-Chairman Management Board Banking

ING strongly supports the objectives of the European Commission for more integrated capital markets. It is important that Europe delivers on these fundamental parts of the Capital Markets Union thereby helping to provide alternative sources of financing and increasing risk sharing and optionality for investors. In this viewpoint we focus on three key elements of the CMU:

- Rebuilding a strong securitisation market supporting the efficient allocation of funds and allowing for the distribution of risk to the right investors.

- Access to financing for SME deserves special attention; the focus should be on i) diversifying financing sources, ii) strengthening the equity base of these enterprises, iii) investing in financial education and literacy and iv) closing the information gap between borrowers and lenders.

- The importance of liquidity in secondary markets.

A well-functioning securitisation market unlocks financing for the European economy

If the banking sector in Europe should deleverage and shrink, while at the same time lending to households and businesses should be maintained, then securitisation is highly instrumental. It has the potential to reduce bank leverage by placing notes with external investors achieving derecognition of underlying portfolios from the balance sheet. This requires solid securitisation structures and a smoothly functioning market, with few regulatory hurdles on both the issuing and the buying end.

After the financial crisis, European markets have become more fragmented. Banks’ issuance of securitisations for funding purposes has dropped significantly as investor demand disappeared because the securitisation product was contaminated. The securitisation technique continued to be applied through large volumes of securitisations retained on the bank’s balance sheet for (contingent) liquidity purposes.

Over the past eight years many European countries have introduced covered bond laws to compensate for the fall-back in securitisation. Consequently, the funding mix of Dutch banks too has moved from RMBS towards covered bonds. These covered bonds however do not allow investors to attract non-recourse exposure to the underlying assets, nor do they free up regulatory capital.

It is therefore very positive that securitisation has moved up on the regulators’ agenda and actions are undertaken to restore its functionality. ING considers it important that all elements are being looked at such as proper retention requirements , an adequate capital treatment to fairly weigh securitisation risk exposures with respect to the underlying assets and convergence between the different regimes for capital treatment of securitisation investments (e.g. Solvency 2 for insurance companies, which currently favours direct exposures to mortgage loans over securitisation investments secured by the same assets).

In the context of CMU, synthetic securitisations are also important; credit risk is transferred to investors by hedging this risk on a specific portfolio. These transactions are conducted solely for risk transfers/capital relief purposes, typically with SME or corporate loans as underlying assets.

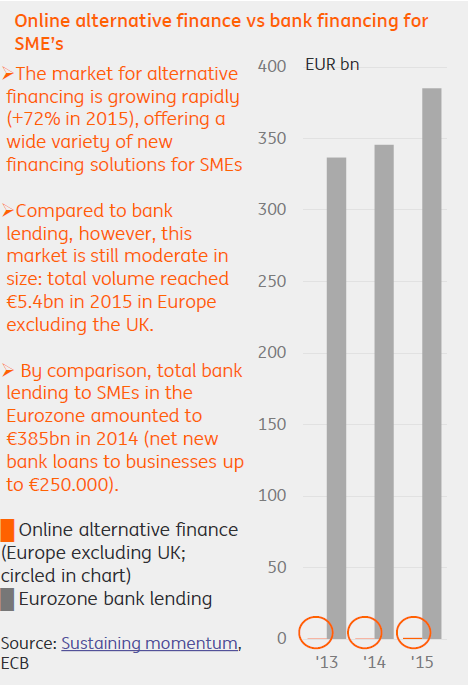

More diversified financing sources for SMEs are needed

Traditionally, European banks have played a dominant role in the financing of SMEs. Recently, new entrants are coming to the market, partly driven by technological change and the search for higher yield by institutional investors and private individuals. The crowdfunding and peer-to-peer lending industry is growing rapidly and creates new internet platforms, where the demand for and supply of SME-loans can be matched.

Yet, ING believes that banks will continue to play a leading role in the financing of SMEs. Banks have the advantages of access to funding, a broad product range allowing one stop shopping, a local distribution network, economies of scale and skills to assess credit and market risks.

The advent of new entrants will increase competition, improve service levels and enhance access to finance for SMEs. However, ING believes that more is needed. The financial crisis has severely weakened the capital base of many SMEs. It has also shown that SMEs are more vulnerable to a slowdown in consumer demand. In addition, there is a structural change in distribution channels due to e-commerce and the life cycle of new products has shortened.

In ING’s view, start-ups and scale-ups are often better served with equity than debt instruments. ING therefore welcomes the efforts being undertaken to promote instruments for equity and/or risk bearing capital for SMEs, such as the Subordinated Loan Fund in The Netherlands1) and by lowering the tax burden on equity and quasi-equity investments.

More focus on financial and business education and literacy can also help to strengthen SMEs and improve their ability to acquire funding from banks and specialized private investors.

Another key factor is the issue of asymmetric information between SMEs and providers of debt and equity financing. In the Netherlands, a program is set up called ‘Standard Business Reporting’ (SBR).2) ING believes that SBR will strongly enhance access to finance for SMEs and will also drive down the administrative costs of reporting. In ING’s view, the European Commission could play an active role in promoting SBR throughout the EU as part of the CMU action plan.

The importance of liquidity in secondary markets

For a good functioning of capital markets there should be sufficient liquidity in secondary markets. Secondary markets have become more illiquid as a result of many factors; in particular the quality of the liquidity on the bond market is very poor. One of the reasons is that banks can take less risk on their books due to the stricter capital rules, the trading book review and other regulatory initiatives like EMIR and MiFID.

Therefore we appreciate the emphasis placed by the EC in its accelerated reform of the CMU action plan to review the current corporate bond markets thereby focusing on market liquidity.

Other considerations when developing a Capital Markets Union

Often references are made to the US, where capital markets play a bigger role in financing the economy. And whilst the ambition for a bigger role of capital markets is positive, one should not too easily pass by the fundamental differences between the EU and the US markets.

(I) First of all there is the variation in accounting standards between EU jurisdictions. Alignment of accounting practices is therefore a crucial element of a CMU.

(II) A cultural difference can be noted: where US investors look for opportunities in case markets get volatile, EU investors are much more inclined to sit on their money and take a wait-and-see approach. So how can capital market practitioners make this money flow, wake up this frozen money.

(III) So far the discussion on the CMU focuses to a large extent on the perspective of the issuers, while capital markets distinguishes three main groups: issuers, investors and intermediaries. In INGs view all three groups should be taken into account in case measures are considered by the EC. Especially the role of intermediaries should not be ignored.

1) See www.nlii.nl

2) The main goal of SBR is to develop a Single Electronic Format for the efficient exchange of relevant business information from SMEs and large enterprises for the purpose of tax filings, depositing annual financial statements at the Chamber of Commerce and providing credit reports to banks or other providers of financing.

See www.sbr-nl.nl/english-site and www.sbrbanken.nl/english