Climate science vs energy security: the new challenges to reaching net zero

This article is a copy of the original article on Think.ing.com

While climate science calls for urgent action to limit global warming to 1.5 degrees Celsius, concerns for energy security will add complexity to achieving a net zero economy. Governments and corporates should find a pathway that best suits them, set interim targets, report progress against these targets, and invest early with a long-term mindset

The recently published IPCC report shows increased concern about climate risks

What a year for energy security, energy transition and climate change

The Russia-Ukraine war – and the consequent energy crisis – has complicated the discussion around the global energy transition and climate change.

The topic of energy security will continue to be important for policymakers, corporate decision-makers, and investors as they plan their pathways toward a net zero economy.

But the Intergovernmental Panel on Climate Change (IPCC) says the routes to net zero are becoming more complex, with its calls for immediate and bold action turning louder each year.

More than one year into the war, and in light of a recently published IPCC report, we examine what the science of climate change means for the global economy, how energy security comes into play, and what that means for the energy transition worldwide.

IPCC report shows increased concern about climate risks

IPCC, an intergovernmental agency of the United Nations, is considered the most authoritative source of scientific assessments of climate change. In March, the organisation released the Synthesis Report of its sixth assessment cycle, which not only provides a comprehensive and evolving analysis of climate science, but also offers recommendations for policymakers. Some of the key messages of this report include:

- The world has already reached 1.1 degrees Celsius of warming compared to pre-industrial levels, which has led to detrimental impacts not seen in human history. This indicates that the door to limiting global warming within 1.5 degrees Celsius of increase is rapidly closing. But luckily, it remains open for now, and to get there, all economic sectors across the world need to be involved in rapid and strong actions to reduce emissions.

- For the first time in its history, the IPCC concludes that the world already has too much unabated fossil fuel production. According to the report, the existing unabated fossil fuel infrastructure is already large enough to deplete the world’s 500 gigatonnes (Gt) of carbon budget – the total amount of carbon dioxide (CO2) allowed to be emitted if we are to keep global warming within 1.5 degrees Celsius with a 50% likelihood of success. The report also finds that current investment in fossil fuels still exceeds that for climate adaption and mitigation. This could add more pressure to negotiations to phase down fossil fuel use at COP28 this year, as well as more pressure for companies with large fossil fuel footprints to decarbonise faster.

- Like last year’s report, the IPCC highlights the essential role of carbon dioxide removal (CDR), as well as carbon capture and storage (CCS), in bringing down global emissions. There is a distinction between the two: although both CDR (e.g. forestation, direct air capture, bioenergy with CCS, etc.) and CCS involve capturing CO2 and storing them underground, CDR results in a net decrease in emissions but CCS does not since it only captures the extra emissions from economic activities. Nevertheless, both methods are highlighted in the IPCC report. The report emphasises that CDR will be essential from now on to bring global emissions to net zero, and CCS is crucial in slashing emissions from fossil fuels and the industrial sector.

There are multiple ways to reach a net zero economy…

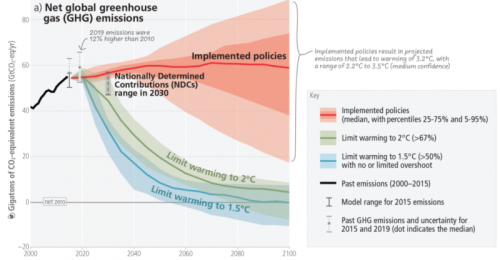

That said, the IPCC has assessed around a hundred scientific pathways that limit global warming to 1.5°C by 2100. It turns out that multiple pathways are possible depending on different technology options. The main technology options are:

- Energy efficiency gains.

- Wind and solar energy.

- Bioenergy.

- Hydrogen and other synthetic fuels.

- CDR and CCS.

The International Energy Agency’s (IEA’s) net zero by 2050 scenario is often seen as the benchmark scenario or pathway. Compared to other scenarios, it relies less on CCS and CDR technologies and more on energy efficiency, renewables and hydrogen. Still, significant amounts of CCS and CDR are needed to reach the net zero target. In fact, there are hardly any scenarios that do without these technologies and those that do rely on extraordinary energy efficiency gains that seem hard to realise.

Whichever pathway they choose, policymakers, corporate decision-makers, and investors should act fast. While the net zero by 2050 goal seems to be far on the horizon, it translates into a 50-60% emission reduction target by 2030. That’s just around the corner, given the long lead time for serious emission reduction programmes.

Acting fast is cost-effective too. The IPCC concludes that “mitigation pathways with early emissions reductions represent higher mitigation costs in the short-run but bring long-term gains for the economy compared to delayed transition pathways”. The report also suggests that taking earlier mitigation action can lead to higher long-term GDP than achieving the same global warming level by 2100 with weaker early action.

IPCC pathways for global greenhouse gas emissions

Source: IPCC report

…but key uncertainties make it hard to predict the optimal pathway

One might think that reaching a net zero economy is simply a matter of implementing the ‘right set’ of the above-mentioned technologies and the policies that support them. Unfortunately, it is much more complicated due to key uncertainties that will drive our future energy systems and economies:

- What role will fossil fuels play in a net zero economy? If fossil fuels continue to play a considerable role, we will rely more on CCS and CDR. If fossil fuels are largely phased out, the energy system will rely more on renewables and synthetic fuels like hydrogen.

- What role will nuclear power play in a net zero economy? If technological breakthroughs such as small module-sized reactors and nuclear fusion emerge, nuclear energy can play a much bigger role in the future energy system. This can also be a push for hydrogen made from nuclear power instead of power from renewables (purple hydrogen instead of green hydrogen). CCS will likely play a more limited role in such a system.

- Will there be large sector shifts in economies across the world? The size of energy-intensive sectors is important. If countries outsource the production of steel, aluminium, cement, plastics, chemicals or fertiliser to other regions, the role of both fossil fuels, CCS and hydrogen could be smaller. On the other hand, they will still want to use these products through imports so the exporting country or region might need to rely more on these technologies.

- To what extent will economies be based on circular principles like the re-design, re-use and recycling of products and materials? For example, hydrogen (instead of coal) could be the main energy source for steel production. And the recycling of steel can be done in smelteries that run on renewable or nuclear power rather than coal or gas-fired ones. Finally, the re-use of steel could reduce the demand for virgin steel.

- What will the international energy landscape look like? For example, will a strong international hydrogen market emerge where Europe can import from regions with lower production costs (like the US, Australia or the Middle East)? And if so, will that hydrogen be green (a push for renewables) or blue (a push for CCS)?

- To what extent will considerations about strategic autonomy influence our future economies and energy systems? It might be beneficial to produce energy in countries where the process is cheapest and cleanest, but is that likely to happen when countries want to become more self-sufficient?

All of this makes it extremely complex to draw the pathway towards a net zero economy. In the medium run toward 2030, more renewable energy, electrification, energy savings, and CCS seem to be no-regret options, at least if one takes a pragmatic and cost-efficient approach towards reducing emissions. From 2030 onwards, the pathway still needs to be discovered and requires more flexibility for climate technology and policy implementation.

Energy security concerns have added to the complexity too

Last year was a special year for climate change, as the world showed us through the Russia-Ukraine war that energy security needed to still play a substantial role along the transition to net zero emissions.

Because of the need to secure short-term energy supply, many governments temporarily turned to non-Russian fossil fuels to power economic activities. For instance, several countries in Europe, including Germany and The Netherlands, had to postpone closing coal-fired plants. China and India were ramping up coal production from existing plants so that they would have more LNG to be exported to Europe at attractive rates. China is even investing heavily in new coal-fired power plants. And because of the turmoil in energy prices, governments worldwide provided more than $1tr of fossil fuel subsidies, the highest ever and roughly twice the amount in 2022. Therefore, in the power sector, global emissions from electricity generation reached an all-time high in 2022.

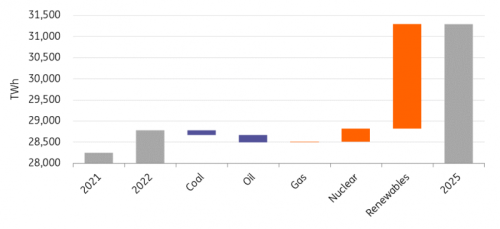

However, 2022 also showed us how governments have been pushing even harder to invest in renewable energy, facilitating a structural change in the energy system to ensure longer-term energy security through clean energy. According to the International Energy Agency, global renewable power capacity increased by 25% in 2022, while the sales of electric vehicles soared by almost 60%. Global renewable power generation is estimated to grow by roughly 2,500 TWh between 2022 and 2025, largely exceeding other sources, with the share of renewable generation rising from 29% to 35%.

Changes in global electricity generation by source, 2021-25

Source: International Energy Agency

The almost paralleled development in the fossil fuels and renewables industries conveys a positive message that governments are indeed linking long-term energy security with their energy transition plans. But before a comprehensive clean energy system is established, fossil fuels will continue to play the role of “a cheap quick fix” whenever something goes wrong. That will add a constant factor of uncertainty to the complexity of climate change combats –a factor that governments, companies, and investors all need to take into consideration.

In the even longer term, the notion of energy security will also evolve as governments race to secure raw material supply for clean energy technologies. This can lead to policies that favour a jurisdiction’s domestic market, which can then result in increased de-globalisation of decarbonisation supply chains. We are already seeing some of this in the US Inflation Reduction Act (IRA) and the EU’s Net-Zero Industry Act, with even more complexities added to the global fight against climate change.

Despite these complexities, both the US and Europe are setting their economies on a path to net zero emissions

US: Difficulty advancing climate ambition, risking reversals

The US has been in a period of heightened green ambition, with the Biden administration having set targets to reduce greenhouse gas emissions by 50-52% compared to 2005 levels, achieve 100% clean electricity by 2035, and reach net zero emissions by 2050.

Since its inauguration, the administration has rejoined the Paris Agreement, reclaimed its active role in international climate negotiation, and passed two key pieces of legislation, the Infrastructure Investment and Jobs Act and the IRA. With hundreds of billions of dollars planned to be spent on improving clean energy infrastructure, incentivising clean energy adoption, and advancing low-carbon technology, the US is already attracting soaring investment along the clean energy value chain. The Biden administration is also proposing stricter regulation standards, such as on automotive pollution, to disincentivise high-emissions economic activities.

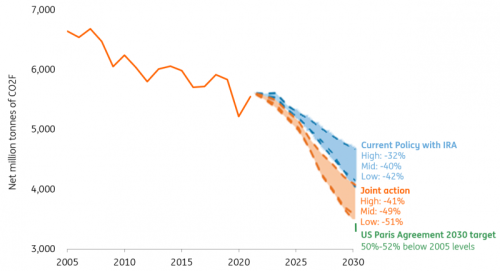

The Biden administration’s green ambition will have a profound impact on the energy transition in the US. It is estimated that the IRA alone, with current policies, will lead to a 32-42% emissions reduction compared to 2005 levels by 2030. If Congress, federal regulators, and states all take aggressive policies, the reduction can be deepened to 41-51%.

Joint action by Congress, federal regulators and states can deepen US emissions reduction from the IRA

US greenhouse gas emissions in net million metric tons of CO2-equivalents

Source: ING Research based on Rhodium Group and Carbon Action Tracker

The high, mid, and low ranges reflect uncertainty around fossil fuel prices, economic growth, and clean energy technology costs.

However, the implementation of these policies does come with challenges and compromises. Since day one of his term, President Biden has been dealing with a delicate balancing act between its climate policy and energy security/market stability considerations. After suspending federal oil and gas leasing in 2021, Biden not only resumed the leasing last year on the back of restricting Russian oil imports, but also released 1m barrels per day of oil to the US’s strategic reserve for six months. Last month, Biden approved the controversial Willow oil drilling project at the National Petroleum Reserve in Alaska – a project that is estimated to be able to produce almost 600m barrels of oil. These are all examples of efforts that have been chosen to ensure energy security alongside all the other climate policies.

Plus, it is uncertain whether this green phase will continue as the country heads into its 2024 presidential election. If Congress becomes controlled by the Republicans, and if a Republican president is elected, then the IRA could be in danger of getting repealed. This can greatly disrupt and delay the US energy transition, although certain areas of clean energy, such as CCS and blue hydrogen, can still get bipartisan support from other channels.

EU broadening the path of carbon pricing for emission reduction

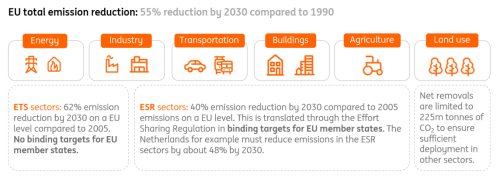

In its latest Fit-for-55 strategy, Europe aims to reduce greenhouse gas emissions by 55% by 2030 compared to 1990 levels, but policy options differ per sector. While the power sector and large manufacturers fall under the Emission Trading Scheme (EU-ETS), the transportation sector, small manufacturers, built environment, agriculture and land use sectors are subject to the Effort Sharing Regulation (ESR) within Europe. This split, and the fact that the EU-ETS started in 2005 and hence does not have 1990 as its baseline, results in different reduction targets. The ETS sectors must reduce emissions by 62%, and the ESR sectors by 40%, both on a European level and compared to 2005 levels. This adds up to 55% of emissions reduction for Europe by 2030 compared to 1990 levels (which is the international benchmark year).

Emission reduction framework and targets differ per sector and country

EU policy framework for emission reduction

Source: ING Research based on CE Delft, Berenschot and Kalavasta

The EU-ETS is a cap-and-trade scheme; it is the main policy instrument to reduce carbon emissions in Europe and in that respect it differs from the US which relies more on tax incentives. Under the EU-ETS, all heavy energy users must hold a number of carbon allowances equal to their yearly emissions. Allowances can be traded and each year the total number of allowances (the cap) is reduced to ensure that the reduction target is met. The carbon price adjusts accordingly. Under the Fit-for-55 package, the yearly reduction of the cap will increase from the current 2.2% to 4.4%. As a result, the carbon price seems to have found a new equilibrium level of €75-100 per ton of carbon, up from €25-30 per ton of carbon prior to the presentation of the Fit-for-55 package.

Corporate decision-makers can apply different strategies within the EU-ETS scheme. The early movers invest heavily in carbon reduction technologies and behaviour, emit less carbon and save on carbon allowances as a result. Others might apply a wait-and-see approach, and need a relatively large amount of carbon allowances for a longer period.

As for the ESR, the regulation results in national reduction targets for the respective sectors. These targets are binding and countries can be punished if they are not met. Note that the ETS mechanism does not result in binding targets for member states. In that sense, some European governments introduce national CO2 reduction targets and legal courts hold on to those targets. This means countries can reach their national target but still get fined by the European Commission if they have not met the reduction target in the sectors of the Effort Sharing Directive. Emissions in the ETS sectors must be kept outside national reduction targets in order to align national and European carbon reduction targets.

Next to these emission reduction targets, the EU makes use of:

- Emission standards for F-gasses in industrial appliances which are used to prevent damage to the ozone layer, but are also powerful greenhouse gases.

- Targets to reduce methane emissions most notably in manufacturing and the oil and gas industry.

- The Renewable Energy Directive (RED) sets targets for renewable energy and synthetic fuels like hydrogen both on a national and sector level.

- The Energy Efficiency Directive (EED) sets targets for energy savings, both on a national and sector level.

- The Energy Performance of Buildings Directive (EPBD) sets binding standards for the energy use of buildings through energy labels.

- Emission standards for transportation modes like cars, trucks, ships and airplanes.

- The Corporate Sustainability Reporting Directive (CSRD) provides sustainability reporting standards for companies and investors.

The individual member states themselves define the policies and instruments to meet these targets. As a result, Europe has a mixed bouquet of subsidies, taxes and regulations that support the transition towards a net zero economy.

Conclusion

The IPCC has made it clear that climate change presents a ‘code red for humanity’ and that urgent actions are needed from all parts of the global economy to drastically reduce emissions. There are many pathways toward net zero emissions by mid-century, but key uncertainties – including the speed of technological advancement, cost perspectives, and policy environments – make it hard to advise on the optimal path, which might also differ per country. Moreover, concerns over energy security have added another layer of complexity, as they can significantly drive a country’s climate policy direction.

Under this context, it has become more important that governments, corporates, and investors set incremental targets to break down their mid-century ambitions, benchmark and report progress against these targets, invest early in long-term efforts, and find out the pathway that works best for them.