Commodities: Europe ends winter with comfortable gas storage

This article is a copy of the original article on Think.ing.com

We have finally reached the end of the heating season and Europe has managed to end winter with storage at record levels for this time of year. The job of refilling storage through the injection season should be much easier, assuming no big supply surprises. Oil prices are likely to trade higher through the year following surprise cuts from OPEC+

Gas Storage Barcelona Spain - Feb 2023 source: Shutterstock

Record-high European gas storage

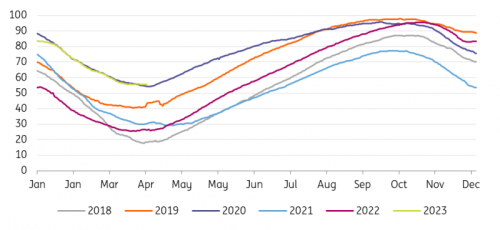

The EU has officially exited the 2022/23 heating season with storage 56% full. This is well above the five-year average of 34% and in fact record levels for the end of winter. We expect the EU to achieve its target of having storage 90% full by 1 November. Given the high storage levels currently, the region will need to see net injections of around 34bcm compared to roughly 67bcm last year. This should be manageable for the region.

Despite the more comfortable gas balance, the EU will need to continue to see demand destruction through 2023. The European Commission recently extended the 15% voluntary demand cut through until the end of March 2024. If the European market was to become extremely tight, this would shift to a mandatory cut. However, demand reductions over the winter have exceeded this. We believe that the EU only needs to see a demand reduction of around 10% from the five-year average from April 2023 onwards.

We now expect TTF to average EUR51/MWh over 2023, having come out of this winter with storage higher than what we were expecting. Meanwhile, significant further downside is likely limited given we are in the coal-to-gas switching range, whilst we still need to see demand destruction through the year (just not as aggressive as seen in recent months).

The key assumptions on the supply side are that remaining Russian daily pipeline flows continue through the year, and that only a partial recovery in Chinese liquefied natural gas (LNG) demand this year leaves adequate LNG supply for Europe. So far, we have not seen a strong recovery from China. LNG imports over the first two months of the year were down 11.9% year-on-year. And at the moment, Asian spot LNG prices are trading at a discount to TTF.

EU gas storage ends winter at record levels (% full)

GIE, ING Research

OPEC+ surprise cuts tighten the oil market

The oil market had a fairly volatile month over March, unable to escape the broader financial market turmoil. This volatility appears as though it will continue into April following a number of OPEC+ members announcing surprise voluntary supply cuts.

A handful of OPEC+ members have announced supply cuts of 1.66m b/d, which will run from May through until the end of 2023. 500k b/d of these cuts are from Russia, which will be an extension of existing cuts that were originally set to end in June. Therefore, real cuts among other producers total around 1.16m b/d. Given that most of these members are producing at or near their current product targets, the actual cuts will be close to the announced cuts.

Clearly, OPEC+ members have not been content with Brent trading in a largely US$70-80/bbl range and want the floor for the market at higher levels. The more modest supply growth from the US would have also likely provided comfort to OPEC+ that it could cut supply and push up prices without the fear of losing a significant amount of market share to US producers.

The announcement to cut supply is a bit of a surprise, given that the market was already expected to tighten significantly over the second half of the year. These additional cuts mean that the market will be even tighter later in the year. As a result, we expect Brent to trade above US$100/bbl over the second half of 2023. We forecast Brent to average US$101/bbl over the second half of the year and US$104/bbl over the fourth quarter.