Global aviation outlook: Air fares climb higher amid the unprecedented recovery of travel

This article is a copy of the original article on Think.ing.com

Demand for air travel is proving resilient despite higher ticket prices. Passengers returned rapidly in 2022 and the recovery will continue this year and next. This is primarily being driven by leisure, but business travel is picking up too. Meanwhile, staff shortages and delivery delays for newly-ordered aircraft are a challenge for airlines

After an unprecedented drop in demand during the pandemic, the aviation sector is now witnessing a significant rebound in leisure travel

A soft landing for global aviation

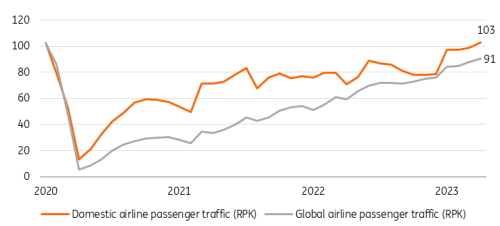

After an unprecedented drop in demand for air travel during the Covid-19 pandemic, the aviation sector is witnessing a significant rebound. Travel figures for the first half of 2023 show that people are eager to fly. Despite purchasing power pressures and a global economic slowdown, people are prioritising previously postponed trips. Strong labour markets are supportive here, as just 10% of the global population in the upper middle and higher income classes are responsible for almost 90% of passenger traffic. Of course, "revenge" travel supported the recovery this year, but without restrictions and health concerns, people seem keen to resume flying more permanently, especially for leisure purposes and family visits. Domestic air travel has recovered the most so far, particularly in the US and India.

Global air traffic has recovered strongly due to pent-up demand

Index global passenger revenue kilometer (RPK) (2019 = 100)

IATA, ING Research, latest datapoint: April

Travel rebound relatively strong

Airlines downsized their global networks of (indirect) connections and destinations over the pandemic, and this hasn’t been restored yet. For European airlines, the number of direct and indirect destinations at airports (connectivity) ended up at 71% of pre-pandemic levels in 2022. This lags behind flight activity (83% on average in 2022), which can be explained by subdued intercontinental and business traffic which is catching up more strongly in 2023.

Airlines have started to reintroduce long-haul destinations and raise frequencies at European airports, but only recently. And, of course, the war in Ukraine and the closure of Russian airspace have also had a negative impact on European connectivity.

European flight traffic continues to recover in 2023

Index flights from and to European countries* (index 2019 = 100)

Eurocontrol, ING Research

*Eurocontrol area, 7dma, last datapoint 06/21

Solid double-digit recovery for aviation in 2023

Bookings suggest that airline ticket demand across large countries and intra-Europe ("domestic") was back to around 100% of pre-pandemic levels in May 2023, while demand for international trips returned to 80% of its 2019 level. On the back of this, we expect the average annual growth for Revenue Passenger Kilometer (RPK) to hit 25% in 2023 compared to 2022. Recovery is set to naturally slow down in 2024 but will continue at a moderate pace. All in all, we expect global passenger travel volume to end up close to 90% of its pre-pandemic level in 2023, with (short haul) domestic travel at the upper end and international travelling at the lower end.

Uneven recovery across regions

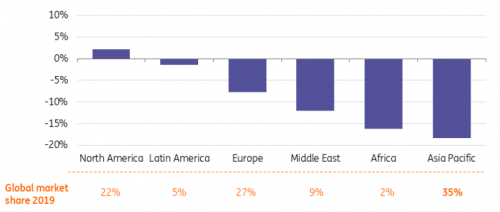

Recovery isn’t equal across geographies. Traffic in the US already exceeded its 2019 level in 2022, but in the Asia-Pacific, (international) traffic is just below two-thirds of its 2019 level. European flight traffic returned relatively strongly and hovered around 92% in June. Low-cost carriers make up a larger share of passenger traffic this year on the back of the leisure travel surge. This was illustrated by stronger bounceback flight activity in countries like Portugal, Spain and Greece in 2022. Ryanair even exceeded pre-pandemic passenger levels by around 15%. This shows that leisure travel has rebounded the strongest.

The world's largest airline market – Asia – has the most recovery potential

Revenue Passenger Kilometer (RPK) per region in April 2023 vs April 2019, and market shares 2019

IATA, ING Research

Air travel to and from China – which finally picked up in the spring of 2023 – will strongly support the further global recovery of passenger traffic. Its global share of domestic passengers stood at 17% of RPK traffic in 2022, down from 25% in 2019. On the international side, the share was just 1% vs 9% in 2019. This implies there is ample opportunity to recover.

Other parts of Asia-Pacific, including Australia and New Zealand, show a delayed but strong recovery as well. All in all, passenger volume in the Asia-Pacific region is expected to surge more than 60% this year compared to its low 2022 base.

The Asian-Pacific market also offers the highest structural growth potential. This is not only driven by population growth but also pushed by the expanding middle class, as flying is strongly correlated with income. Flights per capita are still low compared to advanced countries. Before the pandemic in 2019, the US had 2.8 passengers per capita and the European Union 1.7, compared to 0.5 in China and just 0.1 for India.

Business travel returns, but not yet fully

Despite the cost and time benefits of the working-from-home/remote work trend, business travel has started to return as well. According to aviation analytics firm Cirium, business travel rebounded to 75% of its pre-pandemic level in 2022, with weaker recovery on shorter routes where corporates prioritised alternatives where possible. Airlines see further room for recovery.

The returning demand for wide-body aircraft from carriers is also a sign of sustained recovery in this segment. British Airways – an important airline for business travel – believes this will recover to 85% in 2023. Premium class or business seats are now also filled up by consumers willing to pay extra for more comfort.

No permanent blow for airline traffic, but lower future growth

The resilience of business travel has been underestimated, but nevertheless the pandemic will leave traces. The current rebound is being fueled by business partners seeking to catch up on physical meetings after years of restrictions, and is at least partly attributed to pent-up demand. Meanwhile, long-term growth perspectives are also tempered in the general sense, for three reasons:

- Although business travel is in recovery, remote working and the increase in online meetings will remain part of office work and replace part of business travel.

- Climate awareness is growing among consumers and there are a rising number of sustainability-linked policy measures as airlines align ambitions. Sustainable aviation fuels will start to push up ticket prices, and in Europe carbon prices (ETS) will gradually kick in more strongly the following years. Higher fares won’t hold consumers back from flying, but will probably temper the pace of growth.

- The war in Ukraine and the closure of Russian airspace for the Western world is not likely to end anytime soon and this makes intercontinental flying less efficient. A flight between Frankfurt to Tokyo avoiding Russia is now one-to-three hours longer, which is up to 20% more fuel-consuming. European airlines also have a disadvantage here compared to Chinese airlines. In a broader sense, global geopolitical tensions and headwinds for international trade could drag on air cargo growth and possibly business travel.

All in all, air travel is still expected to see long-term annual growth, but the figure will be closer to 3% than to the pre-pandemic 5-6% for the next two decades, with Europe probably seeing the lowest number.

Capacity is a limiting factor for airlines in 2023 and 2024

The capacity gap in aviation is quickly narrowing with the return of passengers. The load factor – a metric used in the airline industry to measure the percentage of available seating capacity that has been filled with passengers – approached its 2019 level of 82.6% in April 2023. Consequently, pressure on capacity is rising, whereas airlines face delivery delays for newly-ordered aircraft.

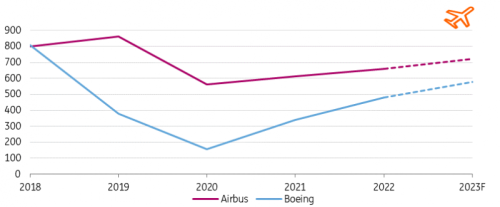

Deliveries of new planes is still significantly lower than pre-pandemic

Number of delivered commercial airplanes by manufacturers Airbus and Boeing

Annual reports, ING Research

Manufacturers slashed aircraft production and aerospace supply chains need time to recover

Supply chain shortages have generally eased, but this isn’t the case yet in the aerospace industry. Aircraft production at Airbus and Boeing has fallen sharply since 2019, while Boeing was already forced to cut production in 2018 because of the grounding of the B737 Max aircraft following software and safety issues. This turned into 1.5 years of missed output up to 2022 and production hasn’t recovered yet. Delivery targets for 2023 are still around 75% of pre-pandemic numbers. Supply chains and aircraft manufacturers need 2023 and 2024, at least, to get fully up to speed. Why is this?

- The aircraft supply chain is complicated with large numbers of components and (certified) suppliers. Ramping up production means all the suppliers down the line need to increase production as well.

- The production of aircraft was initially reduced much more severely than the ordering intake because of interruptions and initial uncertainty about the future of travel. This had repercussions throughout the supply chain.

- Aircraft (parts) manufacturing in small series is labour-intensive and faces shortages of skilled workers.

- High safety standards and related regulations in aviation are restrictive. Components and suppliers need to be certified on behalf of the European Union Aviation Safety Agency (EASA) in Europe or the Federal Aviation Administration (FAA) in the US to comply with safety. This has become important from a legal perspective.

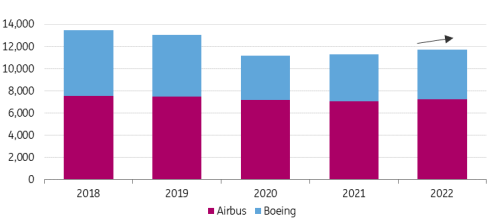

Order intake exceeds aircraft production increase, pushing up backlogs

Orders for new aircraft ramped up in 2021 and 2022. In these years, the total net new order intake of around 1.500 aircraft at Boeing and Airbus equalled its 2019 level. This year also shows acceleration, as the Paris airshow in June generated already orders for 1.250 aircraft. Alongside the struggle to increase production, this means order books remain packed. Based on current production levels, the backlog reaches up to 10 years. Airbus’s 500-plane order by Indian budget carrier IndiGo – the largest order in history – won't be delivered until 2030-35.

Backlog of aircraft manufacturers is increasing after years of low deliveries

Airbus and Boeing order books: number of commercial planes, end of year

Annual reports, ING Research

Delayed aircraft deliveries drags on fuel efficiency progress

The global commercial aviation fleet comprises about 28,000 aircraft in total and is expected to expand significantly over the next two decades. The lagging production figures result in a looming deficit of aircraft. This has revived strong leasing demand, keeping older aircraft such as B777s and A330s, with lessors – companies that lease out their fleet of aircraft to airlines – able to charge higher leasing rates. According to Cirium, parked inventory aircraft was still 5% of the total fleet above pre-pandemic levels in May, but aircraft that are good to go on short notice (an estimated 60%) are returning to service quickly. And there are also still (leased) units stalled in Russia. This means there is still some spare capacity, but this is diminishing fast and varies per aircraft type.

Several airlines have run into limitations because of postponed delivery schedules, including United Airlines, Delta Airlines and Ryanair. The cancellation of flights by airlines such as Transavia in the Netherlands illustrates the tightness of current capacity, as component delivery faces limitations as well.

The delay also has negative implications for efficiency. New generation aircraft are usually 10% to even 25% more (fuel) efficient than their predecessors. Postponed replacements slow reductions of emissions per seat/passenger km for airlines in the years ahead.

Another limiting supply factor is labour shortages in the air as well as at airports

Aircraft capacity is not the only constraint. The airline industry is also facing the challenge of staff shortages; pilots, cabin crew, as well as security, handling, and traffic control staff at airports. This has already held back traffic over the summer of 2022 and the industry still faces hiring issues. Many workers left the industry during the pandemic but vacancies are returning with the rebound. The tight labour market also poses a higher risk of labour conflicts against the backdrop of elevated inflation.

Many airlines have returned to profitability

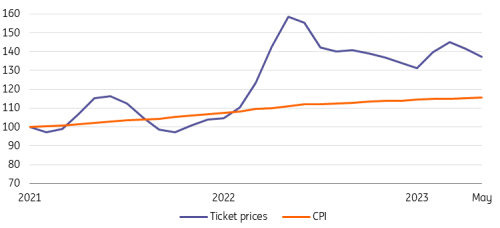

As demand is currently not an issue and supply is limited, pricing power is with the airlines. Capacity constraints, as well as downsized networks (and frequencies), generally push up prices. US airline tickets were more than 30% more expensive in May 2023 compared to January 2022, outpacing consumer prices. Fares have dropped again over the last year, but this can be explained by significantly lower jet fuel prices (making up 20-25% of total operational costs).

The current pricing environment has been rare over the past decade due to continuous price pressures. Current market dynamics support the return to profitability. An increasing number of airlines are set to step up profitability this year. The average operational profitability of the airline sector (EBIT) is expected to recover to 2.8% in 2023, with net profits just above 1%, according to the International Air Transport Association (IATA). US airlines are expected to be the most profitable, supported by strong regional passenger volumes. Asian airlines need more time to return to profitability.

Airline tickets in the US more expensive amid post-pandemic demand rebound

Index ticket prices vs consumer price index (CPI) in the US (Jan 2021 = 100)

St. Louis FED, ING Research

Flying will become more expensive

Capacity tightness currently puts upward pressure on ticket fares. But ticket prices are set to climb structurally.

The traffic and emissions rebound in the aftermath of the pandemic also illustrate the decarbonisation challenge the sector faces. Pushed by policy and public pressure, sustainability is increasingly impacting airline markets. Airlines are investing more in efficiency measures like fleet renewal and many of them have started (joint) sustainable aviation fuel (SAF) production and blending initiatives and committed to corporate targets.

In Europe, in particular, a SAF blend mandate as well as a step up in carbon pricing (ETS) will lead to higher ticket prices in the years to come. The Refuel EU regulation requires airlines to blend 2% SAF by 2025 and 6% by 2030. Airline KLM blended a share of 0.6% SAF in 2022, but the industry average was just 0.3% and this rate will have to be raised. As BioSAF is still two-to-three times as expensive as jet fuel, this will add to total costs.

In addition, the gradual reduction in free carbon allowances from 25% in 2024 to 100% in 2027 means full carbon taxing kicks in in 2027. For a roundtrip from London to Athens (406 kg CO2), this results in a levy of €32.50 to be passed on to customers.

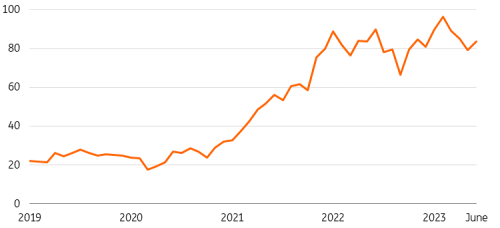

Carbon prices up on the back of reduction of (free) allowances

Carbon spot price Europe (ETS), € per ton

Refinitiv, ING Research

Freight market in reverse

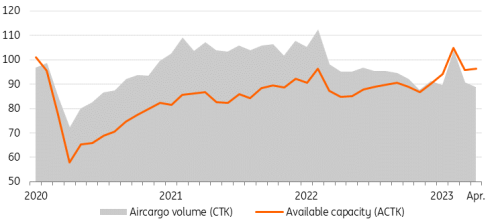

After highly profitable years for air cargo, with global transportation over the pandemic and the circumvention of blocked supply chains, the return to normality came with a setback for airfreight. Belly capacity has returned with the gradual reintroduction of long-haul flights and a range of new freighters added by airlines, but container carriers like Maersk and CMA-CGM, and logistics services providers' capacity, has almost returned in full. At the same time, demand for high-value and time-sensitive (consumer) products has faced a correction.

Freight rates in cargo are still higher than before the pandemic, but with faltering trade growth the peak in air cargo came crashing down in 2023 and 2024. Despite dropped freight rates, cargo activities will still deliver a higher contribution to the revenue of active airlines, but rates remain under pressure. New trade routes and higher capital costs for cargo underway could provide some support for demand in due course.

Airfreight capacity returns while demand slows

Index global development of aircargo volume in ton/km (CTK) and estimated available capacity (ACTK) (2019

IATA, ING Research

How are major European carriers performing?

IAG

IAG reported a strong improvement in financial results for the first quarter of 2023, with total revenue of €5,889m, up 71.4% year-on-year, driven by higher passenger revenues of €5,041m, up 89.9% YoY, and operating profit before exceptional items of €9m, compared to the loss of €741m in the first quarter of last year. According to IAG, robust customer demand, in particular in the leisure segment, allowed the company to generate a positive underlying operating profit in the first quarter for the first time since the first quarter of 2019. The positive results were underpinned by a strong yield performance across individual group airlines and lower total costs per available seat kilometres.

IAG continued to roll out capacity in its core North Atlantic and Latin American markets, which are now back to the pre-Covid 19 levels of capacity, as well as grow Vueling’s network. The company expects capacity to be around 97% of the 2019 levels for the full-year 2023.

Furthermore, the company notes that the outlook for the summer season remains positive, with customer demand remaining strong across all regions, in particular for leisure customers. At the same time, IAG noted that business travel continued to recover more slowly. The company also commented that at this stage it does not have full visibility of customer bookings for the second half of this year, with uncertainties related to the macroeconomic backdrop, including customer confidence, remaining. However, on balance, IAG currently expects its FY23 operating profit before exceptional items to come in above the higher end of the previous guidance range of €1.8bn to €2.3bn.

Lufthansa

Lufthansa Group commented that it was on track with regard to its operational objectives following the release of its first-quarter results. In the first quarter of 2023, the company had revenue of €7,017m, up 40.3% YoY, adjusted EBITDA of €272m (compared to the adjusted EBITDA loss of €32m in the first quarter of 2022) and adjusted EBIT loss of €273m (compared to the loss of €577m in the respective prior year's quarter). During the first quarter of 2023, Lufthansa Group’s airlines carried 21.6 million passengers, up 64.3% YoY. The company also said that demand for the coming months is looking very good, and on the short and medium-haul tourist-focused routes customer demand is already exceeding 2019 levels. For the second quarter, Lufthansa expects capacity of around 82% of the 2019 levels and yields up to 25% above the 2019 levels, with an adjusted EBIT exceeding that of 2Q19 (of €754m).

Based on capacity offered between 85% and 90% of the 2019 levels for FY23, Lufthansa expects a significant increase in adjusted EBIT year-on-year. According to the company, this improvement is underpinned by strong bookings, elevated yields and lower fuel costs.

From a strategy perspective, Lufthansa continues to pursue its multi-airline, multi-hub and multi-brand approach. At the end of May, the company announced an agreement to acquire a 41% stake in Italy’s ITA Airways, expected to be completed by the end of this year.

Ryanair

In May, Ryanair reported results for the financial year ending 31 March 2023. During the reported year, the airline’s revenue was €10,775m, up 124.4% YoY, and operating profit before exceptional items was €1,573m, a major improvement from the loss of €470m in the prior year. Ryanair carried 168.6m passengers in the 12 months to 31 March 2023, up by 73.6% YoY. In terms of outlook, the airline aims to grow the number of passengers carried to approximately 185m in the year to 31 March 2024 (+10% YoY) As is the case with its peers, Ryanair noted that current demand remains robust and peak fares are trending ahead of last year.