How the US is slowly catching up with Europe on ESG and climate policies

This article is a copy of the original article on Think.ing.com

The US and EU are both heading toward tougher regulations on ESG disclosure and standardisation. But there is a contrast between the difficulties America is facing in establishing Environmental, Social and Governance regulations versus the progress made in Europe.

The US is catching up with Europe on green and ESG issues. The US Envoy for Climate, John Kerry, and the EC's Green Deal lead, Frans Timmermans, pictured in 2021

ESG regulation in the financial sector is rapidly evolving. On the one hand, there is growing awareness among investors and companies that higher Environmental, Social and Governance disclosure and standardisation will provide consistent, comparable, and reliable information and help them better judge opportunities and risks in their decision-making processes. On the other hand, concerns are rising over potential policy uncertainties and legal challenges.

In this article, we compare the current ESG regulatory situations in the financial sectors of the US and the EU. We also provide at the end some thoughts on the two jurisdictions' climate policies targeted at economic activities.

ESG disclosure mandates will be evolutional but face strong headwinds

In March 2022, the US Securities and Exchange Commission (SEC) released its long-awaited proposed rules on mandating certain climate-related disclosure for listed companies. Those rules include disclosure of Scope 3 emissions, carbon offsets, and climate-related risks for relevant companies.

After receiving significant comments from various market players, the SEC is expected to publish the final climate disclosure rules this April. Gary Gensler, Chair of the SEC, has signalled that the Commission is considering giving more flexibility to several provisions in the original proposal, including mandatory disclosure of Scope 3 emissions, as well as a requirement to disclose climate costs that are 1% or more of each line-item total of a company’s financial statement.

And the SEC also plans to release disclosure mandate proposals that go beyond climate change. The Commission aims to release proposed/draft disclosure rules on human capital management in April. And it's hoping to publish proposed rules on ESG fund disclosure for asset managers, final rules on fund names, as well as on corporate board diversity.

Despite all that, the final climate disclosure rules may be less stringent than some are hoping for - that all these mandates in the works will lead to higher ESG data transparency, standardisation, and comparability. This can then more effectively allocate capital to companies or projects with higher performance or make more significant progress in managing sustainability.

However, the disclosure proposals remain vulnerable to legal challenges. In June 2022, the Supreme Court ruled that the Environmental Protection Agency (EPA) does not have the authority to put a limit on greenhouse gas emissions from power plants. This ruling sets a precedent for future lawsuits and indeed, in February this year, some Republicans from Congress published a letter arguing that the SEC’s proposed rules on climate-related data disclosure exceed the agency’s authority.

Dividing ESG views in the US can introduce more risks to investors

The US is witnessing an increasingly divided policy environment regarding ESG. Congress recently voted to adopt a resolution that would block a recent rule set by the Department of Labor (DOL) to allow private employer-sponsored retirement plans (ERISA) to consider ESG and climate factors. This is one of the most recent examples of federal anti-ESG efforts from policymakers, with over 600,000 retirement plans worth $12tn in assets under the bill's impact.

In reaction, President Biden vetoed the passed bill, the first veto of his term. But even a veto might not be able to keep the Department of Labor's ESG rule in place. In January, 25 states announced a lawsuit against the Biden administration over the DOL rule. And again, with the 2022 Supreme Court decision setting a precedent, the risk of the DOL rule being overturned needs to be considered.

More than 20 states have proposed or passed anti-ESG bills at the state level. Noticeably, Texas was the first to have passed anti-boycott legislation in 2021 to prevent local entities from conducting business with banks that choose to adopt ESG policies or are divesting from Texan fossil fuel companies. It has triggered other states to follow suit. There are also state-level efforts to reject anti-ESG measures. For instance, Wyoming has just voted down two new pieces of anti-ESG legislative proposals. And the policy fraction is further complicated by several other states proposing or passing bills to support ESG integration in investments.

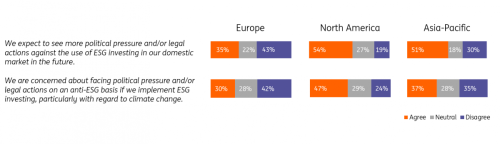

Dissenting standpoints from regulatory federal decision-makers, as well as drastically different ESG regulatory approaches across states, can lead to higher policy uncertainty and more risks of asset owners pulling money out of asset managers. Investors may also find it harder to have a unified strategy without heightened reputation risks. A survey of 300 international and wholesale investors with more than $27tn in assets under management shows that 47% of the investors are concerned about facing political/legal pressure on an anti-ESG basis if they implement ESG investing (versus 30% in Europe and 37% in Asia). 54% of them expect to see more pressure against ESG investing in their domestic market in the future (versus 35% in Europe and 51% in Asia).

Nevertheless, investors and issuers with strong ESG beliefs can still find a way to carry on. Clean energy is an area that will see sustained investment and ESG debt issuance, supported by the Inflation Reduction Act (IRA).

Investors in North America are more concerned about mounting anti-ESG political and legal pressures

To what extent do you agree with the following statements on the role of policymakers and politicians regarding ESG investing, including decarbonisation and other actions to tackle climate change?

Source: Robeco, ING Research

Data may not sum to 100% due to rounding

Fed’s role in addressing climate change risks will stay limited

The Fed Chair Jerome Powell indicated in January that it would play a very limited role in addressing climate change risks in the financial system. It is worth noting that the Fed has taken some action in recent years to address climate change. It joined the Network for Greening the Financial System in 2020, a group of central banks around the world to tackle climate risks in the financial sector. A year later, it created the Financial Stability Climate Committee and the Supervision Climate Committee to start exploring the impact of climate risks on the financial system. Most recently, in January this year, the Fed launched a climate risk stress test pilot programme where six of the biggest US banks were asked to conduct climate scenario analyses by July.

However, it is unlikely that the Fed will take on much more. This contrasts with the European Central Bank's more comprehensive approach. the ECB is not only more advanced in asking banks to manage climate change, it is also incorporating climate change factors into its corporate bond purchases, collateral framework, and so on.

There is still uncertainty regarding the Fed’s limited approach to climate change. For the climate stress test, it remains to be seen if the pilot will be extended to more banks and to what extent that will have capital and portfolio consequences.

An explosion in ESG legislation

The difficulties in the US in rolling out climate-related policies contrast with the progress made in Europe ever since the European Commission published its ambitious Sustainable Finance Action Plan in 2018, enforcing it a year later through the European Green Deal.

The EU Taxonomy regulation (June 2020) is the best-known and most influential piece of legislation adopted by the European Union in the past few years. It sets out a unified classification system to identify environmentally sustainable economic activities. An economic activity is environmentally sustainable under the EU Taxonomy if it substantially contributes to one of six environmental objectives* and does no significant harm to any of the other objectives (together known as technical screening criteria). Additionally, the economic activity must meet minimum safeguard provisions.

The EU Taxonomy regulation is also at the heart of Europe’s far-reaching sustainability disclosures regime for financial and non-financial companies. The Taxonomy regulation introduced additional transparency requirements under the Sustainable Finance Disclosure Regulation (SFDR) (effective from March 2021) to measure the taxonomy alignment of the investment portfolios of fund managers. Large and listed companies that publish non-financial information under the Non-Financial Reporting Directive (NFRD) also must make disclosures on the taxonomy alignment of their eligible economic activities. The Corporate Sustainability Reporting Directive (CSRD) (effective from January 2023) extends the scope of the NFRD disclosure requirements to all large companies (EU and non-EU) and listed SMEs. Taxonomy compliance is also the core prerequisite under the upcoming voluntary EU Green Bond Standard.

Disclosures on Taxonomy alignment are only the tip of the iceberg when it comes to Europe’s sustainability reporting regime. For the SFDR, asset managers must also disclose whether their products promote environmental or social characteristics (so-called Article 8 or light green products), invest in an economic activity that contributes to an environmental or social objective (Article 9 or dark green products), or have neither one of these two purposes (Article 6 or non-green products). Besides, they should monitor the principal adverse impact (PAI) on sustainability factors and publish due diligence policies related to them. The PAI statements cover 18 mandatory indicators and at least two of the 46 additional indicators. They provide, for instance, information on exposures to companies active in the fossil fuel sector or on the share of investments in companies involved in violations of the UN Global Compact principles or OECD guidelines for multinational enterprises.

The CSRD, in turn, ensures investors have access to sufficient information to perform their due diligence analysis for SFDR purposes. The CSRD not only extends the scope of the non-financial reporting requirements to a broader group of companies, including listed SMEs, but it also introduces far more detailed sustainability reporting requirements than those applicable under the NFRD. For one thing, the CSRD requires companies to disclose transition plans, confirming that their business model and strategy are compatible with the 1.5°C global warming target of the Paris Agreement and the 2050 climate neutrality objective of the EU Climate Law.

While revealing its climate action plan, the European Central Bank (ECB) also aims to make CSRD compliance central to its collateral acceptance by 2026. After all, it will take some time before all CSRD disclosure details are in place and applied. The first set of sector-agnostic European Sustainability Reporting Standards (ESRS) is expected to be adopted by the European Commission in June this year. However, the European Financial Reporting Advisory Group (EFRAG) will still have to draft the sector-specific standards in the coming three years.

* Climate change mitigation, climate change adaptation, the sustainable use and protection of water and marine resources, the transition to a circular economy, pollution prevention and control, and the protection and restoration of biodiversity and ecosystems.

Executing Europe’s ESG ambitions is not without hurdles

The implementation of the ambitious climate agenda in Europe is for sure not without hurdles either. Putting detailed ESG regulation in place is one thing; being able to meet all the regulatory requirements to the regulator’s intention is something else. The applicable challenges in the field of data availability are very well known. The spiderweb of sustainability regulations created is also leading to numerous interpretation complexities. These are keeping regulators and market participants on their toes in drafting and tracking questions and answers relevant for clarification.

The recent reclassifications by many asset managers of their investment funds from Article 9 to Article 8 for SFDR purposes are a good example. Article 9 funds should, in principle, only make sustainable investments under the condition that no significant harm is done to any environmental or social objective and good governance practices are followed by the investee companies. However, fund managers have interpreted the requirements for sustainable investments differently. Several media reports raised eyebrows last year regarding the number of funds claiming to be Article 9 compliant while still being exposed to fossil fuels or other polluting activities despite the 'do no significant harm' requirements. This has led to questions, including from the European Parliament, regarding the need for clearer minimum requirements for Article 9 fund classification. Against this backdrop, and with the level 2 provisions of the SFDR entering into force at the start of this year, many asset managers decided to be safe rather than sorry and downgraded several funds to Article 8 to avoid greenwashing accusations.

On that same ground, it also remains to be seen how keen issuers of green bonds will be in marketing full compliance with the future European Green Bond Standard (EuGBS). The European Green Bond Standard is a voluntary standard available to all issuers (EU and non-EU) committed to financing environmentally sustainable investments. However, EU green bonds can, in principle, solely finance economic activities that are taxonomy compliant. Companies willing to issue EU green bonds would therefore have to comply with the taxonomy’s technical screening criteria (TSC) and do no significant harm (DNSH) criteria, such as those set by the June 2021 EU Climate Delegated Act.* Particularly when it comes to meeting the 'do no significant harm' provisions, issuers tend to feel reluctant to claim full Taxonomy alignment other than on a best-effort basis. Besides, bonds issued under the EuGBS must meet detailed pre- and post-issuance disclosure requirements subject to mandatory review. Issuers must also include a statement of issuance under the EuGBS and the green bond factsheet in the prospectus.

When it comes to addressing greenwashing concerns, it is also interesting to note that the European Commission published its proposals for a Green Claims Directive on 22 March to protect consumers against false environmental claims.

* The recent provisional agreement on the EU Green Bond Standard provides some flexibility to allocate 15% of the proceeds to Taxonomy-related activities for which no technical screening criteria have yet been established.

The impact of Europe’s sustainability regulations will stretch beyond Europe

Those who think that Europe’s far-reaching ESG regulations will only impact European companies alone should think again. The clearest example is the Corporate Sustainability Reporting Directive, which subjects third-country companies with securities listed on EU-regulated markets to similar disclosure challenges as their European counterparts over a similar timeframe. This includes reporting on the Taxonomy alignment of their economic activities. Moreover, third-country undertakings with substantial activities within the EU must also comply with targeted European sustainability disclosure standards, albeit on a different time scale (only per 2029), subject to fewer conditions but also with an option of reporting via their non-EU parent entity if the EU deems sustainability reporting standards equivalent with such parent company’s country.

Non-EU companies can also voluntarily make use of the EU Green Bond Standard if they want to access EU investors. EU investors would likely consider this to be of great added value as they could count such bonds as 100% Taxonomy compliant for their Taxonomy KPIs (Green Investment Ratios). Non-EU companies aiming to issue an EU green bond would have to meet the strict use of proceeds, disclosure and mandatory review requirements of the standard. As such, they would have the challenge of proving that their green bond proceeds are allocated to assets that are Taxonomy aligned.

Europe recently reached a provisional agreement on the EU Green Bond Standard. Once the final deal is published, it will be interesting to see if, to what extent and over what timeframe, third-country Taxonomies might be used under an equivalence regime, as per the initial proposals of the European Parliament. The environmental objectives, criteria for substantial contribution, significant harm and minimum safeguards should, in that case, most likely be comparable in ambition to the EU Taxonomy.

Conclusion

Both the US and the EU governments are set to implement more robust ESG regulation policies for the financial sector, but the two jurisdictions differ in terms of policy environment, depth and breadth.

In the US, despite the Biden administration's and the SEC's efforts to mandate ESG-related disclosure for eligible listed companies, the country faces a fragmented policy environment, both at the federal and the state levels, where anti-ESG movements have been on the rise. This may lead to longer timeframes for ESG policy implementation or even the reversal of already-established policies, which will add uncertainties and risks to investors and companies.

In the EU, the policy environment on ESG regulations is relatively more unified, leading to smoother policy evolvement. Moreover, the EU has a more complex ESG regulation system, where disclosure requirements (SFDR and CSRD), the sustainable activity classification system (Taxonomy) and the Green Bond Standard work together and reinforce each other. However, in Europe, complying with all the new regulatory requirements also does not come without the necessary data and interpretation difficulties.

That said, there is still hope for the US to catch up with the EU in terms of ESG regulation; the biggest concern is that the progress will not happen as fast.

Where do the US and the EU stand on climate policies?

Now that we have discussed the ESG policies for the financial sector, where do the US and the EU stand on the climate policies that can have significant effects on their economies?

While the US has faced challenges in ESG regulation, it passed the landmark law, The Inflation Reduction Act (IRA) which will substantially spur clean energy project development and attract investment from overseas. Nevertheless, the IRA is rather focused on incentives, and the US lacks stricter regulations and punitive measures to control emissions.

The EU’s climate policy is more comprehensive in design. With the overarching European Green Deal, the EU has established and updated a wide range of policy frameworks, such as emissions standards and renewable energy directives, among others. The EU also has a mature emissions trading system, where emissions caps are set, and a price is put on carbon dioxide. Moreover, the EU recently launched proposals for a Net-Zero Industry Act and the European Critical Raw Materials Act, largely to level the playing field with the US’s IRA, but since it remains unclear how much funding there will be and where it will come from, the incentives these policies raise will likely be not as high as those of the IRA.

That said, the positive note is that the US and EU are now in competition for stronger energy transition and climate policies, which we expect can lead to faster technology advancement and more rapid clean energy adoption in both regions. But there are risks of de-globalisation in clean energy value chains if the two jurisdictions’ policies stay more favourable toward domestic producers and consumers.

And both regions still need to do more to drive their economies more effectively to net-zero emissions. For instance, for the EU, there are still no sector-specific transition paths to give companies guidance on which steps to take to meet the -55% and net-zero targets. For the US, many more efforts are needed beyond mere incentives.