ING posts 2Q2019 net result of €1,438 million

Amsterdam,

- ING continues to record growth in primary customers and core lending

- Retail primary customers rose in 2Q2019 by 300,000 to 12.9 million; total retail customer base reaches 38.6 million

- Net core lending in 2Q2019 grew by €7.4 billion; net customer deposit inflow amounted to €11.7 billion

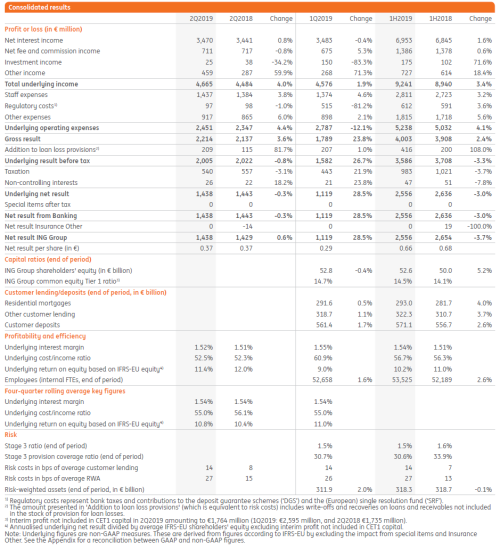

- ING 2Q2019 underlying pre-tax result of €2,005 million; ING declares interim cash dividend of €0.24 per share

- Result reflects well-diversified loan growth at resilient margins, despite margin pressure on customer deposits, as well as stable fee income and a relatively low level of risk costs

- Four-quarter rolling underlying ROE was 10.8%; ING Group CET1 ratio remained robust at 14.5%

CEO statement

“We achieved good results in the second quarter, with solid profitability and healthy growth in both lending and deposits. We added more than 300,000 primary customers in 2Q2019, which demonstrates that our customer experience continues to be differentiating and drive growth,” said Ralph Hamers, CEO of ING Group. “Higher volumes and resilient lending margins supported earnings despite the ongoing low interest rate environment. Looking ahead, we expect that persistently low interest rates will put pressure on net interest income.

“We took further steps in the second quarter to improve the way we manage non-financial risks. The number of FTEs working in KYC-related activities, including our global know your customer (KYC) enhancement programme has increased to over 3,000. File enhancement and transaction look-back operations are resulting in improved reporting of suspicious or unusual activity to authorities in various countries. Our increased focus on KYC and our efforts to streamline our operations are leading to an increased number of accounts that are being closed, including inactive accounts or accounts of which the customers were insufficiently responsive to information requests. And we have started a re-evaluation of certain client and business relationships. We’re also working on promising tools that use machine learning and artificial intelligence to increase the effectiveness of our KYC operations. At the same time, we welcome steps by the Dutch and other authorities to achieve wider cooperation between banks, law enforcement and regulators on both a national and European level to strengthen the financial system’s resilience in the fight against financial economic crime.

“We continued to innovate to improve the digital customer experience and to strengthen our mobile-first approach. In Germany and Poland, we now offer features that help customers to better manage their money by notifying them of upcoming payments, similar to the ‘Kijk Vooruit’ feature in the Netherlands. We’ve enhanced the experience of our mobile app users by adding Apple Pay in the Netherlands, Romania and Spain. Interhyp, ING’s independent mortgage brokerage platform in Germany and Austria, which offers access to over 450 mortgage lenders, had a record quarter and is on track for a 10% market share in Germany.

“We empowered customers through new beyond banking services that help them stay a step ahead in life and in business. Within our global partnership with AXA, we’ve launched our first products in two countries.

“The 26 sustainable bond transactions and 12 sustainable loan transactions in 2Q2019 showed that ING’s commitment to sustainable and green financing is achieving good commercial results. Among them we supported a €750 million green innovation bond for Philips and a €1.55 billion loan to Merlin Properties, Europe’s largest sustainability improvement loan for the real estate sector. And ING is one of the founding banks of the Poseidon Principles, which aim to reduce greenhouse gasses from shipping by 50% by 2050, aligning our shipping financing with our Terra approach.

“We are making good progress transforming our business so we can continue to deliver a differentiating customer experience. At the same time, we took important steps in the second quarter to strengthen our management of non-financial risks, particularly in the areas of KYC and anti-money laundering. We are committed to maintaining the highest standards in these areas, now and in the future.”

Analyst and investor conference call

1 August 2019 at 9:00 am CET

+31 (0)20 531 5821 (NL)

+44 20 3365 3209 (UK)

+1 866 349 6092 (US)

Live audio webcast at www.ing.com

Please use any browser except Internet Explorer to access the webcast through this link

Media conference call

1 August 2019 at 11:00 am CET

+31 (0)20 531 5871 (NL)

+44 203 365 3210 (UK)

Live audio webcast at www.ing.com

Please use any browser except Internet Explorer to access the webcast through this link

Note for editors

For further information on ING, please visit www.ing.com. Frequent news updates can be found in the Newsroom or via the @ING_news Twitter feed. Photos of ING operations, buildings and its executives are available for download at Flickr. Footage (B-roll) of ING is available via ing.yourmediakit.com, or can be requested by emailing info@yourmediakit.com. ING presentations are available at SlideShare.

ING PROFILE

ING is a global financial institution with a strong European base, offering banking services through its operating company ING Bank. The purpose of ING Bank is empowering people to stay a step ahead in life and in business. ING Bank’s

53,000 employees offer retail and wholesale banking services to customers in over 40 countries.

ING Group shares are listed on the exchanges of Amsterdam (INGA NA, INGA.AS), Brussels and on the New York Stock Exchange (ADRs: ING US, ING.N).

Sustainability forms an integral part of ING’s strategy, evidenced by ING’s ranking as a leader in the banks industry group by Sustainalytics. ING Group shares are included in the FTSE4Good Index and in the Dow Jones Sustainability Index (Europe and World), where ING is also among the leaders in the banks industry group.

IMPORTANT LEGAL INFORMATION

Elements of this press release contain or may contain information about ING Groep N.V. and/ or ING Bank N.V. within the meaning of Article 7(1) to (4) of EU Regulation No 596/2014.

ING Group’s annual accounts are prepared in accordance with International Financial Reporting Standards as adopted by the European Union (‘IFRSEU’). In preparing the financial information in this document, except as described otherwise, the same accounting principles are applied as in the 2018 ING Group consolidated annual accounts. All figures in this document are unaudited. Small differences are possible in the tables due to rounding.

Certain of the statements contained herein are not historical facts, including, without limitation, certain statements made of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to a number of factors, including, without limitation: (1) changes in general economic conditions, in particular economic conditions in ING’s core markets, (2) changes in performance of financial markets, including developing markets, (3) potential consequences of the United Kingdom leaving the European Union or a break-up of the euro, (4) changes in the fiscal position and the future economic performance of the US including potential consequences of a downgrade of the sovereign credit rating of the US government, (5) potential consequences of a European sovereign debt crisis, (6) changes in the availability of, and costs associated with, sources of liquidity such as interbank funding, (7) changes in conditions in the credit and capital markets generally, including changes in borrower and counterparty creditworthiness, (8) changes affecting interest rate levels, (9) inflation and deflation in our principal markets, (10) changes affecting currency exchange rates, (11) changes in investor and customer behaviour, (12) changes in general competitive factors, (13) changes in or discontinuation of ‘benchmark’ indices, (14) changes in laws and regulations and the interpretation and application thereof, (15) changes in compliance obligations including, but not limited to, those posed by the implementation of DAC6, (16) geopolitical risks, political instabilities and policies and actions of governmental and regulatory authorities, (17) changes in standards and interpretations under International Financial Reporting Standards (IFRS) and the application thereof, (18) conclusions with regard to purchase accounting assumptions and methodologies, and other changes in accounting assumptions and methodologies including changes in valuation of issued securities and credit market exposure, (19) changes in ownership that could affect the future availability to us of net operating loss, net capital and built-in loss carry forwards, (20) changes in credit ratings, (21) the outcome of current and future legal and regulatory proceedings, (22) operational risks, such as system disruptions or failures, breaches of security, cyber-attacks, human error, changes in operational practices or inadequate controls including in respect of third parties with which we do business, (23) risks and challenges related to cybercrime including the effects of cyber-attacks and changes in legislation and regulation related to cybersecurity and data privacy, (24) the inability to protect our intellectual property and infringement claims by third parties, (25) the inability to retain key personnel, (26) business, operational, regulatory, reputation and other risks in connection with climate change, (27) ING’s ability to achieve its strategy, including projected operational synergies and cost-saving programmes and (28) the other risks and uncertainties detailed in this annual report of ING Groep N.V. (including the Risk Factors contained therein) and ING’s more recent disclosures, including press releases, which are available on www.ING.com. (29) This document may contain inactive textual addresses to internet websites operated by us and third parties. Reference to such websites is made for information purposes only, and information found at such websites is not incorporated by reference into this document. ING does not make any representation or warranty with respect to the accuracy or completeness of, or take any responsibility for, any information found at any websites operated by third parties. ING specifically disclaims any liability with respect to any information found at websites operated by third parties. ING cannot guarantee that websites operated by third parties remain available following the publication of this document, or that any information found at such websites will not change following the filing of this document. Many of those factors are beyond ING’s control.

Any forward looking statements made by or on behalf of ING speak only as of the date they are made, and ING assumes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information or for any other reason.

This document does not constitute an offer to sell, or a solicitation of an offer to purchase, any securities in the United States or any other jurisdiction.

Press enquiries

Raymond Vermeulen

Head of Media Relations & Issues Management, Retail Banking Benelux, corporate governance

+31 20 576 63 69

Send e-mail

Investor enquiries

ING Group Investor Relations

Send e-mail