Synthetic fuels could be the answer to shipping’s net-zero goals, but don’t count on them yet

This article is a copy of the original article on Think.ing.com

Synthetic fuels could be the technology fix that shipping needs because they promise the possibility of reaching zero-emission targets. But they’re costly and lose more energy than fossil fuels. However, as the world tries to reach net-zero goals, shipping companies may have little choice but to use them more; after all, there are very few alternatives.

Making global shipping more sustainable is a far from simple task

Shipping's hard-to-abate sustainability dilemmas

Here’s the dilemma: shipping accounts for 90% of goods transported around the world, and it’s also the most energy-efficient mode of international freight transport. But it’s also a major source of global greenhouse gas emissions. Greener alternatives are often viewed as prohibitively expensive in a highly competitive market. And change is often desperately slow.

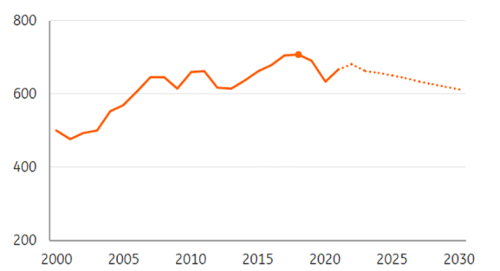

Today, international shipping accounts for 681 million tons of CO2 every year. While the sector is improving in terms of energy efficiency, emissions are likely to stay at about 600 megatons as seaborne trade is expected to grow by 15% by 2030. So, we’re going to look at the business case of synthetic shipping fuel as a technology fix to reduce carbon emissions. We’ll assess where we are right now and the pressures companies are under to meet net-zero targets. And we’ll examine which alternative fuels could be front-running technology as science improves and adapts.

It’s worth adding that we’re working with the consensus view of expected demand for shipping against the current policy backdrop.

Global emissions from international shipping in megatons of CO2-equivalents

Carbon dioxide emissions peaked in 2018 but are expected to remain above 600 megatons of CO2 by 2030

ING Research based on IEA and Clarksons

Shipping is a ‘hard-to-abate’ sector. That's where it's prohibitively costly, or the technology's just not there yet to meaningfully reduce harmful emissions. For instance, the full electrification of maritime shipping is not a feasible strategy, given the technological limitations. So any transition pathways are gradual and long. And the international nature of maritime shipping doesn't help much. You can argue that any policy intervention should be globally aligned and implemented by the global authority, the International Maritime Organization (IMO).

Unfortunately, the IMO is not exactly a fast-moving beast. It's still targeting a 50% reduction in CO2 for shipping by 2050 from a 2008 base rather than from 1990, where the Paris Agreement looks at. That's far away from both the 2015 agreement and the net-zero target for the global economy.

On the other hand, it is encouraging to see some large container liners such as Maersk, MSC, and Hapag Lloyd are already committing themselves to net zero emissions by 2050.

Three ways to reduce emissions

Given these technical and policy limitations, there are three main strategies to reduce emissions:

- Tempering the demand for shipping, which basically means reducing growth in international trade. For example, through nearshoring and the transition towards a circular economy which aims to lengthen the life cycle and duration of consumer goods and to recycle goods locally.

- Improving the efficiency of current bunker fuel engines and vessels

- Apply a technology fix by replacing fossil fuels with biobased and synthetic fuels

We absolutely underscore the importance of demand reduction in sector pathways towards a net zero economy, in particular in hard-to-abate sectors like shipping and aviation. But we also realise that it is not the most likely route given the consensus view for growth in maritime shipping, which is linked to global GDP and population growth.

Furthermore, efficiency improvements in practice tend to stop the growth in emissions but do not reduce emissions in a way that sets the sector on a net zero pathway.

Lastly, the supply of biobased fuels is likely to be limited given the vast amount of shipping fuel that needs to be replaced and the fact that net-zero pathways for other sectors rely on biofuels too (such as aviation, road transport and the chemical sector).

We believe that synthetic fuels are likely to be a crucial ingredient of the transition pathway of maritime shipping towards a net-zero economy. And we're going to explain why.

A technology and fuel fix with synthetic fuels

Today, outside the emission control areas, VLSFO (Very Low Sulpher Fuel Oil) and HFO (Heavy Fuel Oil), in combination with an installed scrubber, are the main fuels used by large marine vessels. HFO is the remnant from the distillation and cracking process of crude oil. It contains compounds such as sulfur and nitrogen. The use of HFO, therefore, has several environmental impacts. Besides being a large emitter of CO2, it also emits polluting compounds such as sulfur and black carbon. So, you have the policy dilemma of trying to decide which pollution to reduce.

We focus on the Paris Agreement's goal to limit global warming to 1.5 degrees Celsius. Since limiting global warming is all about reducing the level of global carbon emissions, the shipping industry also needs to decarbonise. This calls for the transition to synthetic fuels that emit no or little CO2 from well to wake.

Apart from HFO, there are other oil-based fuels ships use. They include Marine Gasoil (MGO), Very Low Sulphur Fuel Oil (VLSFO) or Ultra Low Sulphur Fuel Oil (ULSFO, which are obligatory in emission control areas like the North and Baltic Seas). Liquid Natural Gas (LNG) is an emerging fuel, which is an alternative and ‘cleaner’ fuel compared to oil-based fuels, but it's still a fossil fuel that emits CO2.

Many new ships being built today are being designed to be highly energy efficient, and IMO regulations are playing their part here. Many vessels are also making the switch to operate on LNG to reduce emissions. But it's not a permanent solution and is seen more as an intermediate step towards full decarbonisation of the shipping industry.

This is where synthetic fuels come into play. Synthetic fuels are made in a chemical plant through a chemical process rather than being mined from the earth and refined. Ideally, this production process wouldn't involve fossil fuels (the green route).

In this article, we are going to shed light on the production costs of synthetic fuels (well-to-tank cost) and the use case of synthetic fuels in shipping (tank-to-wake costs). Given the current state of technology, methanol, ammonia and hydrogen are considered relevant synthetic fuels in shipping. The table at the end of this article describes these fuels.

Remember, these fuels are not just theoretical concepts. In the past six months, there has been a range of orders for methanol-capable and methanol-ready vessels in container shipping. These are dual-fuel vessels, able to switch to green methanol after a future retrofit. Maersk, for example, has 19 such vessels on order.

The magic of synthetic fuels in shipping

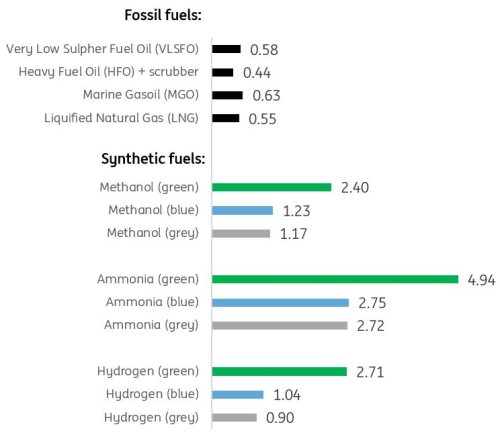

When traditional fossil-based marine fuel is burnt in the engine of a ship, carbon atoms (C) react with the oxygen in the air (O2), which delivers energy and creates CO2. This option is often seen as the ‘black' or 'dirty' technology’ that increases carbon emissions and contributes to global warming. As an indication, oil-based fuels emit 3.5 to 3.7 kilograms of CO2 per dead weight tonnage per kilometre. A similar ship on Liquified Natural Gas saves about 30% of carbon emissions but still emits 2.7 kilograms of CO2 per kilometre.

Indicative emissions per fuel type in kg/DWT/km

Synthetic fuels such as hydrogen and ammonia can drastically reduce carbon emissions in shipping, especially if they are produced with green electricity (green) or when Carbon Capture and Storage is applied (blue)

ING Research

Indicative emissions for a 82.000 deadweight tonnage ship with 230 sailing days per year at an average speed of 17 knots. The CCS capture rate in the production of blue hydrogen is assumed to be 80%. Green hydrogen is assumed to be fully produced with renewable electricity (solar, wind or hydro power) or with zero carbon sources such as nuclear power. We show emissions per unit of distance per amount of cargo so that numbers are comparable across fuel types.

The magic of synthetic fuels is that carbon emissions from ships can be drastically reduced or even nullified in the case of hydrogen-propelled vessels or ships that run on ammonia. And that's especially true when the hydrogen needed to produce ammonia is produced with electrolysers that fully run on renewable power (the darkest green hydrogen).

Methanol is made from syngas, which is a mixture of hydrogen and carbon monoxide and thus still contains carbon atoms (see the appendix table at the end of this article). Ships that run on methanol still emit CO2. Our calculations indicate that emissions are reduced by about 20% compared to oil-based fuels if the methanol is fully green (that's to say, it's produced with green hydrogen and 100% renewable power). When the methanol is produced with blue hydrogen, the vessel emits about 13% less CO2 on a net basis.

Synthetic fuels must be produced in a sustainable way

Note too that LNG emits less than green and blue methanol, but the standard view is that natural gas – and hence fossil-based LNG - should be phased out in a net-zero economy and therefore is a ‘transition fuel’. That should equally apply to methanol as it emits more carbon emissions than fossil-based LNG. In the future, synthetically produced LNG (also called E-LNG) could be part of the fuel mix in shipping, but we'll be looking at that another day.Note too that LNG emits less than green and blue methanol, but the standard view is that natural gas – and hence fossil-based LNG - should be phased out in a net-zero economy and therefore is a ‘transition fuel’. That should equally apply to methanol as it emits more carbon emissions than fossil-based LNG. In the future, synthetically produced LNG (also called E-LNG) could be part of the fuel mix in shipping, but we'll be looking at that another day.

Finally, note that grey ammonia and grey methanol are actually much more polluting than fossil-based marine fuels. The production of synthetic fuels is bound by physical laws that imply high energy losses. As a result, the climate impact of synthetic fuels is worse compared to fossil fuels unless they are produced in a more sustainable way (that is, with blue or green hydrogen instead of grey). It's fair to say that the shipping sector can actually make things worse if it uses synthetic fuels in a non-sustainable way.

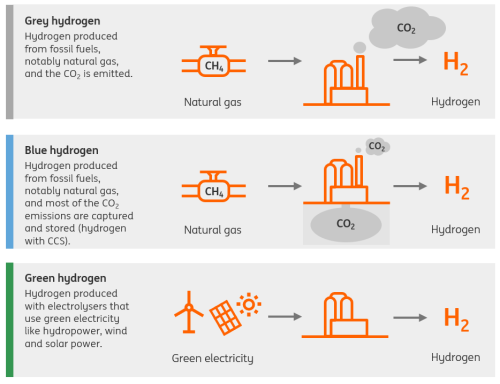

Different methods of hydrogen production

Hydrogen for synthetic fuels in shipping must be blue or green to reduce or eliminate carbon emissions

ING Research

Green synthetic fuels can be nearly ten times more expensive

So, it is clear by now that synthetic fuels can radically 'green' the hard-to-abate shipping sector and put it on a pathway to net-zero emissions. The necessary condition is that the required hydrogen is produced with few carbon emissions, so with blue or green hydrogen.

The obvious questions then are, why hasn’t it already happened? And why aren’t we using synthetic fuels in ships already?

The answer is pretty simple. The technology is still in its infancy, and the production process is very energy intensive compared to conventional fuel, even with mature technology. Therefore, production costs of synthetic kerosene are much higher. Currently, the green options increase fuel costs by 4 to 9 times compared to fossil-based fuels, the blue options increase fuel costs by 2 to 5 times.

Green synthetic fuels are currently a lot more expensive compared to fossil fuels

Indicative unsubsidized cost of shipping fuels in euro per dead weight tonnage per 1.000km (euro/DWT/1.000km)

ING research based on energy prices from Refinitiv and fossil fuel prices in shipping from Clarkson

Fuel costs for a 82.000 deadweight tonnage ship with 230 sailing days per year at an average speed of 17 knots. Fossil fuels costs are based on market prices as of early April 2023. Synthetic fuels costs are calculated based on a gas price of €45/MWh, a power price of €140/MWh, CO2 price of €100/ton, an oil price of $80 per barrel and a euro/dollar exchange rate of 1$=0.926€. Note that this represents the Northwest European energy market as of early April 2023. It also represents (more or less) market expectations on energy prices for 2023 and 2024 in future markets as of early April 2023. The CCS capture rate in the production of blue hydrogen is assumed to be 80%. Green hydrogen is assumed to be fully produced with renewable electricity (solar, wind or hydropower) or with zero carbon sources such as nuclear power. Note that these numbers only represent the fuel costs of shipping, not the total cost of shipping which would include all capital and operational expenses of ships. We are not able to calculate the total cost of ships that run on the respective synthetic fuel as most of these technologies are still in the pilot phase and not available for large ships. Also, most synthetic fuels in shipping cannot be blended with fossil fuels as easily as in aviation.

This price differential is very important for ‘dual fuel vessels’ that can run on synthetic fuels like methanol or ammonia and fossil fuels with minimum adjustments. For these ships, it remains an option to switch to burning fossil-based bunker fuel if it is not during a trip, then at least between trips.

There are two ways of looking at this large price difference:

One way is to say that synthetic fuels are currently too expensive. This can partly be solved with subsidies and innovation, as hydrogen production costs could come down. There are many studies out there that predict large cost declines for green hydrogen. But these only emerge if capital costs for electrolysers decline strongly, power prices reduce and carbon prices increase further. That’s not unthinkable, but also not yet a done deal. It might also be that clients are willing to pay a premium for green shipping, but it remains to be seen to what extent container shipping rates will be impacted.

It is almost impossible to predict the future competitiveness of synthetic fuels in shipping

One could also say that fossil-based fuels are currently too cheap and synthetic fuels are not in a ‘fair fight’. The EU Fit for 55 package starts to address this point by extending the EU Emissions Trading System (ETS) to maritime transport. This pricing of carbon emissions will narrow the cap between fossil fuels and synthetic fuels, in particular the green and blue ones. And the EU carbon border adjustment mechanism might trigger other regions in the world to tax carbon in shipping, too, so that they can use the tax revenues themselves instead of paying the carbon cost to Europe, for instance.

But the price of fossil fuels will also heavily depend on the pricing strategies of oil-producing countries. And we don't know how these countries will respond during the energy transition. Will they flood the market with oil in anticipation of lower oil demand, making it harder for synthetic fuels to compete with fossil fuels (the green paradox)? Or will they be able to keep prices high by reducing production in a coordinated way, which is needed to close the price gap with synthetic fuels?

Given these big uncertainties, it is almost impossible to predict the future competitiveness of synthetic fuels in shipping. And those routes which do exist shouldn't necessarily be relied on to guide as to what may happen many years from now. Shipping companies will be watching these developments closely and should be thinking in price scenarios rather than exact forecasts.

The indirect cost of synthetic fuels as less cargo can be shipped

Synthetic fuels also pose a not-so-nice trade-off between fuel costs and freight revenues. While synthetic fuels could have a positive climate impact in terms of lower CO2 emissions, they come with lower energy densities, especially on a volumetric basis.

The poor volumetric physics of synthetic fuels means that ships that run on them have to install bigger tanks to travel the same distance, but that implies less space for cargo and lower revenues. Or they could ship the same amount of cargo with a similar tank size, but then they have to refuel more often. And since the ship is docked while refuelling, it does not make money by shipping cargo around the world.

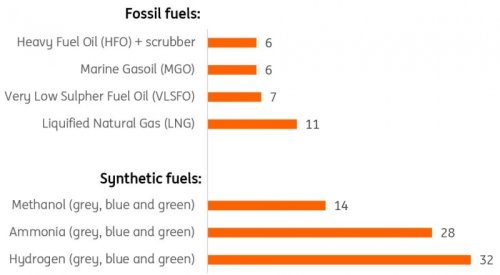

Our calculations indicate that vessels that run on methanol would have to tank 2 to 2.5 times more often compared to vessels that run on HFO, MGO or VLSFO (14 times during the year compared to 6-7 times). Note, however, that the number is pretty similar to ships that run on LNG.

The picture is even worse for vessels that run on ammonia or hydrogen. Due to the chemical characteristics, they have to tank about five times more often if they install a similar tank size compared to vessels which run on oil-based fuels. But tanking around 30 times a year is not a realistic option, so the tank size for ammonia and hydrogen-propelled vessels needs to be larger, which implies less space for cargo if the ship size stays the same.

Synthetic fuels require ships to refuel more often given a certain tank size

Indicative number of yearly refuels*

ING Research

*Number of yearly refuels for our reference ship of 82.000 deadweight tonnage with 230 sailing days per year at an average speed of 17 knots. The benchmark ship runs on HFO and needs to refuel 6 times a year given its tank size. We have calculated the amount of refuels for this tank size for every fuel type. The tank size holds less energy if it is filled with synthetic fuels and therefore needs to refuel more often. Note that all synthetic fuels are liquified.

4 reasons not to hype synthetic fuels in shipping

It's important not to get carried away. Synthetic fuels clearly will be part of a net-zero pathway, in particular for hard-to-abate sectors such as shipping and aviation especially as the ‘easy technological solutions’ such as electrification and end-of-pipe solutions such as Carbon Capture and Storage hold little promise. But we can’t take it too easy, there are downsides as well.

The problem with synthetic fuels is that they have to be made compared to fossil fuels which can be found in the ground. And that production process is very energy intensive. For example, around 65% to 50% of energy is lost in the production process of methanol and ammonia (production efficiency). And about 45% to 60% of energy is lost by burning the fuel in the ship engine (propulsion efficiency). Taken together, you end up with overall efficiencies of 20% at worst and 25% at best, meaning that up to 80% of energy is lost when synthetic fuels are used. Put differently, ships that run on synthetic fuels only use 20%-25% of the energy that is provided. That’s a staggering low performance.

Synthetic fuels require a lot of green hydrogen and thus green electricity from wind turbines and solar panels. In the Netherlands, for example, more than 100 gigawatts (GW) of offshore wind energy is needed to substitute all the oil-based bunker fuels for aviation and shipping with synthetic fuels. Currently, only 3 GW are installed, which is expected to grow towards 20 GW by 2030 and 70 GW by 2050. While these are very ambitious targets for offshore wind, they still fall short of what would be needed for shipping and aviation. And other sectors want to use green electricity too, such as steel making, the plastics industry, road transportation and commercial and residential real estate. So, the low energy efficiencies of synthetic fuels are only justified when green energy is abundant in a net-zero economy, and we're certainly not there yet.

Synthetic fuels not only require green hydrogen, but some (like methanol) also require green sources of carbon. Currently, fossil fuels are an abundant and cheap carbon source, but they won’t really be around in a net-zero economy. As a result, green carbon sources will be scarce in a net-zero economy and must come from biomass, waste (recycling of plastics and food) and carbon reservoirs (underground reservoirs from CCS activities or the air by using Direct Air Capture). All these sources are not yet readily available and commercialised. So, the production of large amounts of synthetic fuels is likely to face fierce competition for green carbon sources with other sectors at best, or competition for carbon shortages at worst.

Given the energy inefficiencies and the likely shortages of green sources of carbon, it might be better to produce blue instead of green methanol. Why would one produce green hydrogen and combine it with a green carbon source, while the methanol can be produced directly from an abundant fossil carbon source and its emissions can be reduced with CCS? Our emissions graph shows that green and blue methanol has about the same emission levels, and both emit less than the fossil-based fuels that are currently used, except for LNG. So while ship owners like Maersk or their large clients such as Ikea, Amazon and Unilever might have a preference for green solutions to position themselves as sustainable companies, a bit of energy-systems thinking might lead to other choices (for example, blue options that remain fossil-based).

At least some potential pathways are becoming clearer

So while synthetic fuels can be produced in a green way, they won’t fly simply because they are green. Synthetic fuels have to beat the incumbent fossil technology, but that won’t be a slam dunk, given the poor physics and economics of synthetic fuels. Therefore, we find it hard to envision a future in which synthetic fuels fully replace fossil fuels in marine shipping.

That does not mean their future role will be marginal either. After all, there are very few other zero-carbon options for marine shipping available other than bio-fuels, of which the supply will be limited. Zero-carbon shipping simply means zero-carbon fuels! That’s why synthetic fuels will be part of the sector’s pathway towards a net-zero economy, but to what extent is yet hard to anticipate.

Finally, policy developments are likely to push for synthetic fuels too. The European Union aims to reduce the greenhouse gas intensity by 80% in 2050 compared to 2020 levels, starting with 2% in 2025. And the IMO is facing mounting pressure to raise its ambition to reduce carbon emissions. That will also mean that shipping will be forced to start using low-carbon fuels.

To conclude, synthetic fuels come with higher costs. The direct costs of higher fuel prices and the indirect costs of more frequent refuels or less cargo that can be shipped. Hence shipping rates need to be higher for vessels that run on synthetic fuels. Secondly, fossil fuels damage the climate, but they are often superior in terms of chemical characteristics. In that regard, they are hard to beat.

It’s still too early to say when shipping will become verifiably sustainable. Even today, the routes to zero emissions are unclear. And they're expensive. But at least we can see a potential path to a cleaner maritime industry, even if we can’t say when we’ll get there nor which of the available synthetic fuels will finally become dominant. Shipping will need to rely on a multi-pronged approach, starting with energy efficiency and one which includes biofuels and Liquified National Gas, if it's going to make good progress.

Appendix: an economist's guide to marine fuels

Fuels in shipping and their main characteristics from an economist’s perspective

Heavy Fuel Oil (HFO)

HFO is the residue of the distillation and cracking process of crude oil. It must be heated at 40 °C during storage to prevent it from becoming ‘a solid substance’ that cannot be burnt in ship engines. Heavy fuel oil has a relatively high sulphur content compared to other types of fuel, and the sulphur is emitted with the ship's exhaust gas in the form of sulphur dioxide (SO2), which is harmful to living organisms and can contribute to acid rain. Therefore, exhaust gas cleaning systems (commonly referred to as ‘scrubbers’) are added to the vessel to reduce sulphur emissions.

The oil price and energy losses in the production process are the main economic parameters of the business case. Marine shipping is not subject to a carbon price.

Marine Gas Oil (MGO)

MGO is also a residue of the distillation and cracking process of crude oil, but unlike HFO it does not have to be heated during storage.

The oil price and energy losses in the production process are the main economic parameters of the business case. Marine shipping is not subject to a carbon price yet.

Very Low Sulfur Fuel Oil (VLSFO)

Also referred to as ‘0.5% Sulfur compliant fuel’ is a fuel that causes less sulfur emissions compared to HFO and MGO.

HFO, MGO and VLSFO have about the same specific and energy density of about 40-42 MJ/kg and 900-1,000 kg/m3. This makes these fossil fuels superior from a chemical point of view: a lot of energy can be derived from a small amount of fuel. Apart from carbon emissions, they are hard to beat.

The oil price and energy losses in the production process are the main economic parameters of the business case. Marine shipping is not subject to a carbon price yet.

Liquified Natural Gas (LNG)

LNG is a colourless and non-toxic liquid which forms when natural gas is cooled to -162ºC (-260ºF). The cooling process shrinks the volume of the gas by 600 times, making it possible to store and ship safely. In its liquid state, LNG will not ignite. When LNG reaches its destination, it is turned back into a gas at regasification plants. LNG is now emerging as a cost-competitive and cleaner transport fuel, especially for shipping and heavy-duty road transport.

LNG has a higher specific density compared to HFO, MGO and VLSFO (50 MJ/kg), but its energy density is 50% lower (~450 kg/m3), meaning that LNG needs bigger tanks to derive the same level of energy compared to oil-based fuels.

The natural gas price, liquefaction, transportation, and gasification costs are the main drivers of the business case. Marine shipping is not subject to a carbon price yet.

Hydrogen

Hydrogen is one of the smallest, simplest and most abundant atoms in the world. It is estimated to contribute 75% of the mass of the universe. On Earth, vast numbers of hydrogen atoms are contained in water, plants, animals and humans. But while it’s present in nearly all molecules in living things, it’s very scarce as a standalone gas. This means that hydrogen needs to be produced by chemical processes. There are three main production processes, all denoted by a colour:

- Grey hydrogen is produced from natural gas, which is a fossil fuel. The carbon emissions are not captured, enter the atmosphere and contribute to global warming.

- Blue hydrogen is also made from natural gas, but up to 85% of the emissions are captured and stored or utilised, a process called CCS. Hence, blue hydrogen has a much lower climate impact than grey hydrogen.

- Green hydrogen is not made from fossil fuels but by splitting water (H2O) in hydrogen (H) and oxygen (O2) through an electrical current. The process is called electrolyse and is completely carbon-free if it runs on renewable electricity like wind, solar and/or hydropower.

Hydrogen has a high specific density of 120 MJ/kg but an extremely low energy density of just 40 kg/m3, meaning that you need large tanks to store the gas. The energy density can be improved to 71 kg/m3 by the liquefaction of hydrogen. Since this happens at -252 °C, it requires a lot of energy, and still the energy density remains low compared to fossil-based marine fuels.

The natural gas price (grey), carbon price (grey and blue) or power price (green) and energy losses are the main cost drivers.

Ammonia

Ammonia (NH3) is produced by combining nitrogen with hydrogen and hence does not involve fossil fuels. The process is called the Haber-Bosch process and operates under high temperature and pressure and therefore requires a lot of energy. Compared to other fossil fuels, the energy density is relatively low. Grey, blue and green ammonia refers to the use of grey, blue and green hydrogen to produce ammonia. The energy density of ammonia is much better than hydrogen (840 versus 40 kg/m3), and hence ammonia is often regarded as a carrier to transport hydrogen. However, ammonia is a highly toxic liquid, so transportation is not without risks. Environmental pollution can be devastating when things go wrong.

The natural gas price (grey), carbon price (grey and blue) or power price (green) and energy losses are the main cost drivers.

Methanol

Methanol is a widely used alcohol that is a feedstock for many different commodity chemicals, such as plastics, but it can also be used as a shipping fuel. Methanol is made from syngas, or synthesis gas, which is a mixture of hydrogen and carbon monoxide. Since there is more hydrogen present in syngas than is consumed for methanol production, an additional reaction takes place where CO2 is added to the system to react with the remaining hydrogen. This CO2 enters the atmosphere again when methanol is burned in a ship engine.

The environmental impact depends on the way the CO2 is sourced. If the CO2 is utilised from CCS activities, the process is ‘carbon neutral’; the shipping sector emits the carbon that is captured in other segments of the economy (like manufacturing). If the CO2 is taken directly from the air through direct air capture or DAC, the process is ‘net zero’ as the shipping sector emits the carbon that was taken out of the air first.

Depending on the source of hydrogen in the syngas, methanol can also be labelled as grey, blue or green methanol.

The natural gas price (grey), carbon price (blue) or power price (green) and energy losses are the main cost drivers.

Methanol can be further turned into dimethyl ether (DME) which can also be used as an alternative fuel in diesel engines due to its high cetane number. But since it requires adding production stages, the economics tend to be worse compared to using methanol.